abluecup/iStock via Getty Images

Arbitrage and mean reversion trades are good ways to capture alpha without overexposing yourself to general market trends. Long-short strategies can try and capture this spread. Alternatively, you can simply move your money in an almost identical security with a lower risk (keeping return constant), or higher return (keeping risk constant). We have done this both ways, and today we go over one example for a REIT we have previously covered several times.

Safehold Inc. (NYSE:SAFE)

If you have been on Seeking Alpha for any length of time, the REIT needs no introduction. Born just prior to the ultimate bubble of ZIRP (Zero Interest Rate Policy), the REIT sucked in many with the promise that they were not building land anymore. So owning land and the building on top (in give or take 90 years) should prove to be a great strategy. Lost in that discussion was whether one should pay anywhere close to these multiples.

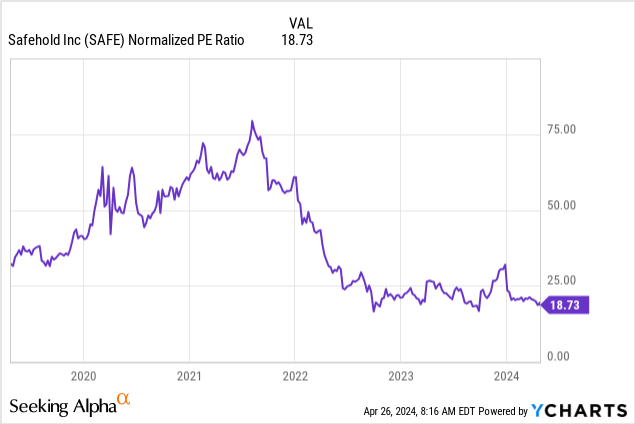

As the REIT has now been “grounded”, investors are less likely to get another shock. Last time around we had suggested that the stock was due for a move over $20, before resumption of the longer term trend.

If we had to guess here, we would think SAFE makes it over $20 at some point soon. The catalyst likely could be lower interest rates as that has been one of the most one-sided boats we have seen.

Source: The Ultimate SWAN Dive

SAFE did indeed move well over $20 and then fell back to $18.50.

Q4 2023

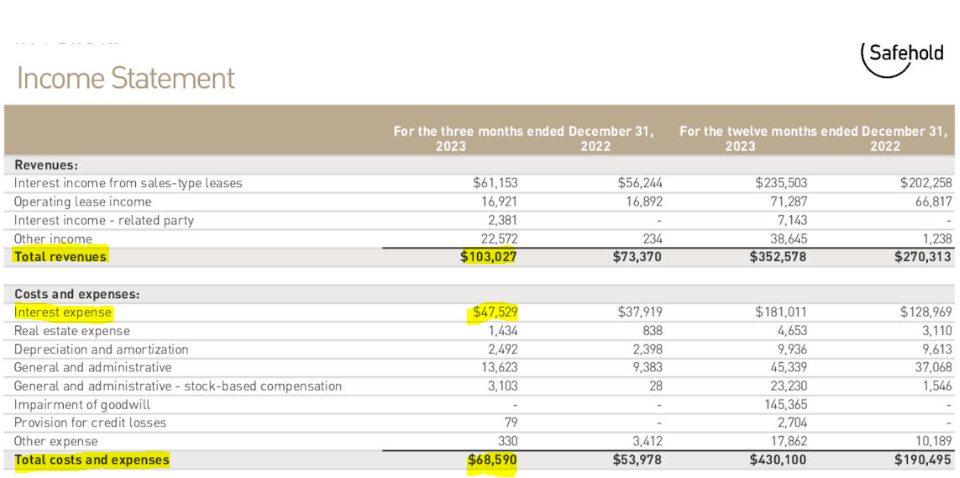

One of the key issues facing SAFE was the relentlessly rising interest expense and Q4-2023 was no different. Interest expense climbed to $47.5 million and was up 25% year over year. In the picture below it appears that revenues have kept pace, but that revenue number contains $22.5 million of “other income” (gains from asset sales).

SAFE Q4-2023 Presentation

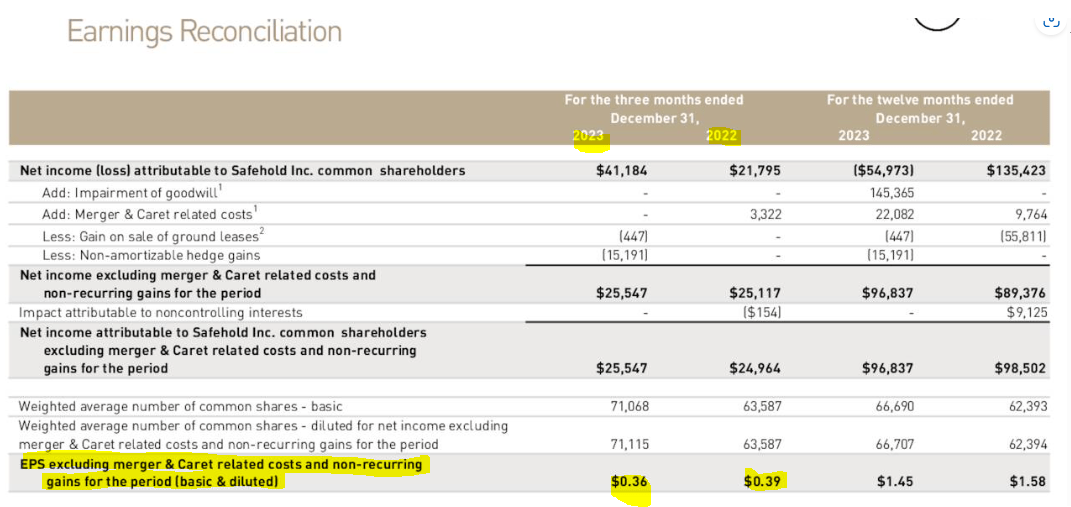

A more normalized measure removing out those gains as well as reducing merger related expenses, shows that normalized EPS declined from 39 cents a share to 36 cents a share.

SAFE Q4-2023 Presentation

While there are many reasons to not be bullish on SAFE, our preferred reason is that the earnings estimates have not aligned with reality. Below are the earnings numbers for the next three years. They are stated as funds from operations (FFO) but they are actually EPS estimates.

Seeking Alpha

You can note two things above. The first being that they have been declining over the last six months and the second that they are far above the annualized Q4-2023 number. Yes, there have been recent investments made and those will produce cash in 2024. But the numbers are far from reality in our opinion. We think they are still pricing in 4-6 rate cuts in 2024 which will ease pressure on SAFE’s floating rate exposure. We are aligned with the low estimate for 2024 and the REIT is likely to disappoint substantially.

Seeking Alpha

Income Anyone?

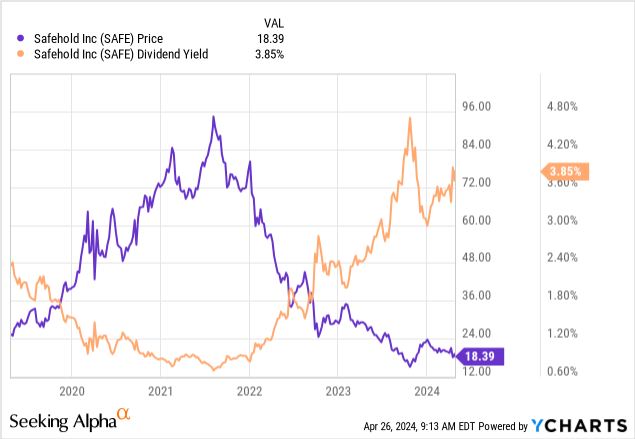

We are now a bit removed from the comical days of 2021 when the promise of owning a single-tenant office building for your great grandchildren allowed you to accept 0.6% yield from a REIT.

At 3.85%, you have to recognize that you are now actually getting paid to wait. Certainly, those betting a deflationary bust and the potential for lower interest rates (and capital appreciation) must be taking notice.

New Bonds

While SAFE may work out here at near $18.00 if interest rates go down, we have always suggested that their bonds may be a better way to get the same return profile. With SAFE’s common, you get 3.85% yield and possibly 2-3% annual appreciation from here. With the bonds, you get that 6% yield to maturity but with far lower risk. Now, the two bonds that SAFE had the bulk of their returns tied to capital appreciation. Their coupons were low and hence income investors stayed out, even though their yield to maturities were fairly decent. Well, investors today have a new alternative.

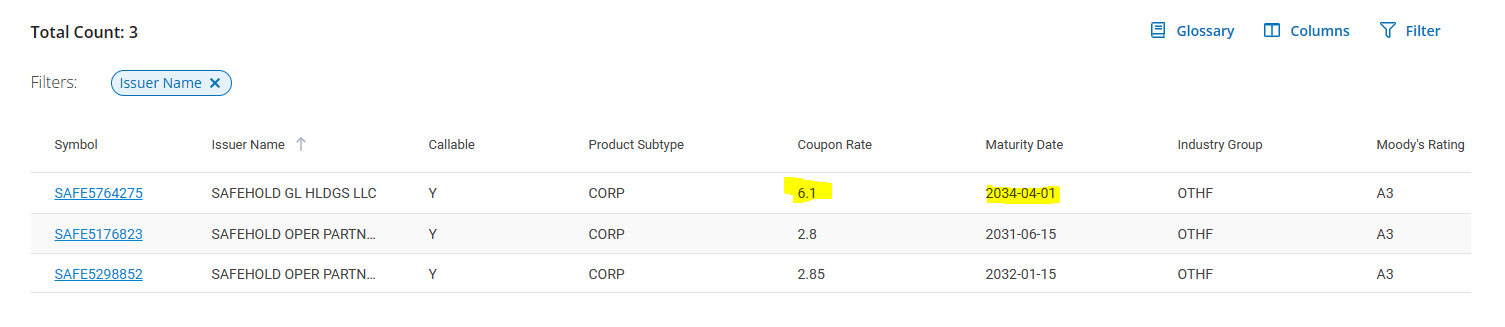

Below are the SAFE bonds along with the stock. The last one there, is the latest SAFE bond.

Interactive Brokers April 25, 2024

Here is another way to see the same data from FINRA.

FINRA

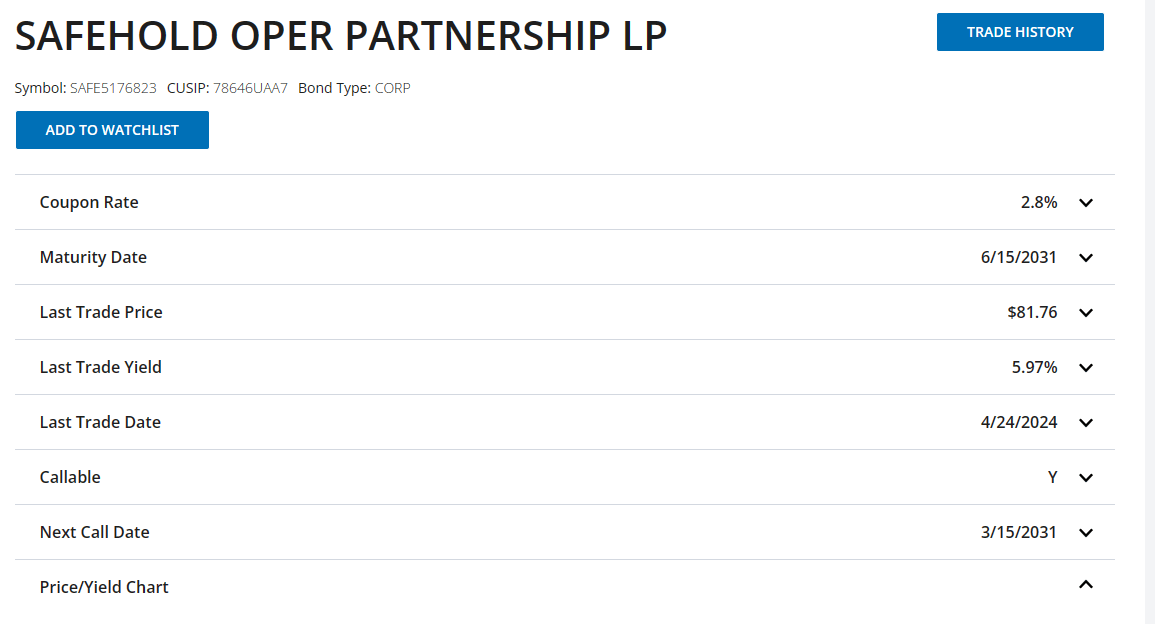

There are two notable things here with these new bonds. First, we are getting a far bigger coupon. Second, these bonds have the highest yield to maturity despite that relatively massive coupon. 2031 bonds shown in the picture have a roughly 6% yield to maturity.

FINRA

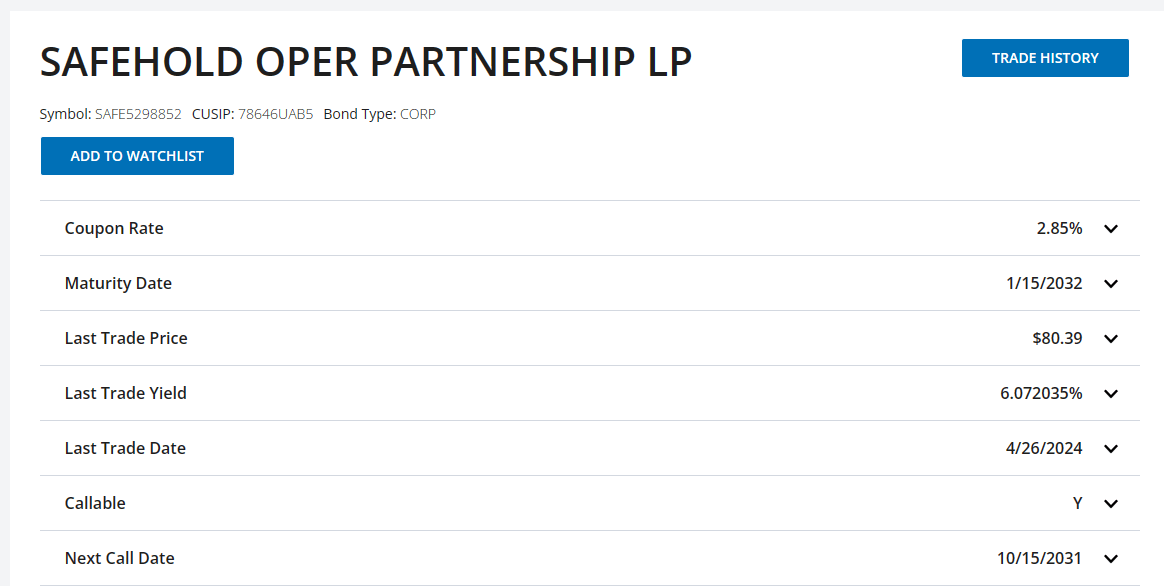

The 2032’s have a slightly better deal on offer.

FINRA

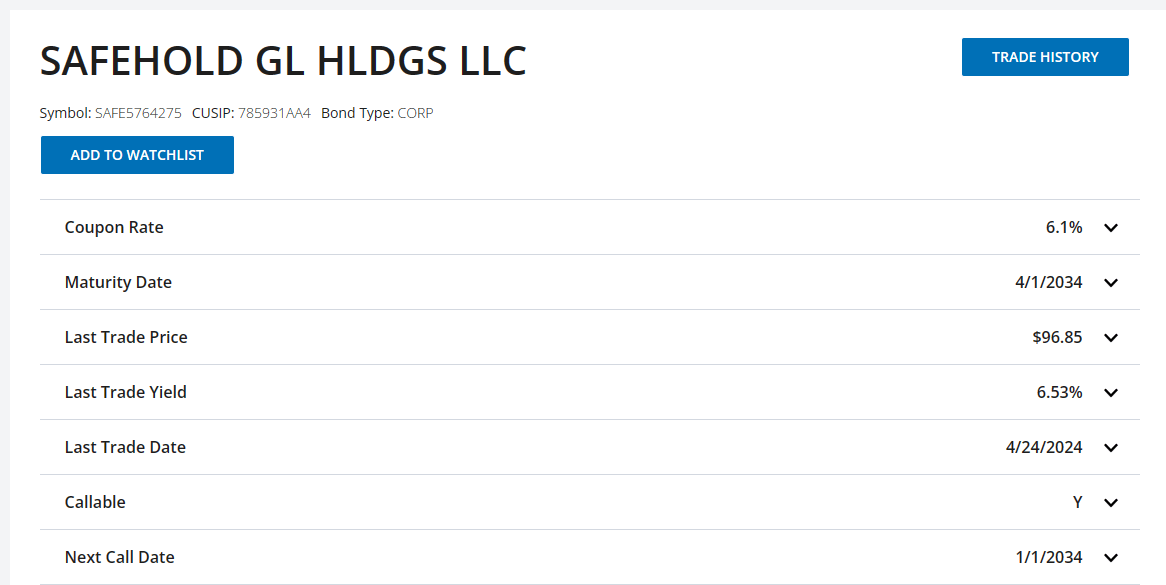

The 2034’s, i.e. the newest bonds, have a 6.53% yield to maturity.

FINRA

Since they are below par, an early call will only enhance your yield to maturity.

Verdict

Moody’s rates these bonds as A3 as they believe the underlying land/ground lease makes SAFE bonds, extremely safe. If you buy that thesis and the credit rating, then these bonds make a lot of sense. They are also, as shown above,…

Read More: Are The 6.6% Yielding A Rated Bonds A Safehold? (NYSE:SAFE)