It’ll take years to get this mess cleaned up, at the expense of investors, landlords, and banks.

By Wolf Richter for WOLF STREET.

Availability rates in the office sector of Commercial Real Estate (CRE) are not getting any better, and in many markets, they’re getting still worse and are hitting new records, as landlords and lenders grapple with waves of massive repricing, with office tower values, those towers that have sold, plunging by 40%, 50%, 60%, 70% and more. Numerous landlords, from Blackstone on down, have let buildings go back to lenders to let them deal with the mess.

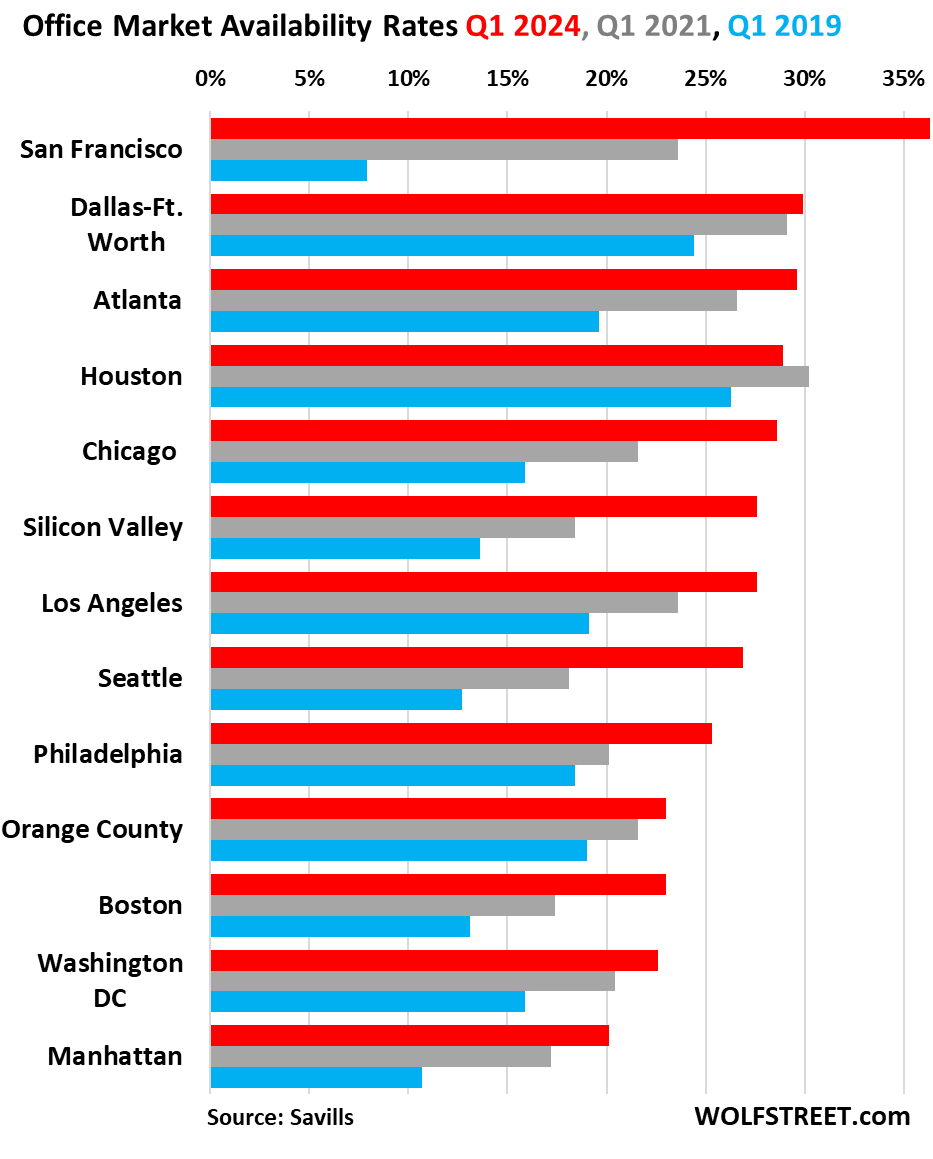

Here is a chart of the 13 markets for which Savills released the Q1 data today, showing the availability rates of office space, so that’s the space that has been put on the market for lease either by the landlord directly or by a tenant as a sublease. Red shows the availability rates for Q1 2024; gray for Q1 2021, and blue for Q1 2019, which were the Good Times.

While San Francisco’s availability rate edged down from a record 36.7% in Q4 2023, to 36.3% in Q1 2024, it remained the worst office market in the US, followed by Dallas-Fort Worth and Atlanta, both at or near 30%. Houston was for years the worst office market in the US, with availability rates of 30%-plus. With the oil boom over the past couple of years, it edged away from 30%.

New worsts. Availability rates in nine of the 13 office markets in the chart rose to new records:

- Atlanta: 29.6%

- Chicago Downtown: 28.6%

- Silicon Valley: 27.6%

- Los Angeles: 27.6%

- Seattle: 26.9%

- Philadelphia: 25.3%

- Boston: 23.0%

- Washington D.C.: 22.6%

- Manhattan: 20.1%

The Good Times for office CRE was 2019 (blue in the chart) and before. In 2019, for example, San Francisco was still the hottest office market in the US, with an availability rate of 7.9%, amid a super-hyped “office shortage” that caused every square foot of office space to be instantly “nabbed,” as the media liked to say at the time to promote the CRE promo-hype further, such as in, “Sony PlayStation nabs big chunk of S.F. building,” or infamously “Facebook nabs first urban office in downtown San Francisco,” 436,000 square feet of office space spread over 33 floors of a high-end tower, the “181 Freemont,” for up to 3,000 Facebook employees someday, god willing, the biggest office lease signed in three years at the time. A year ago, Meta put it on the market as sublease. Now TikTok is talking to Meta about leasing three of the 33 floors.

Obviously, asking rents are not coming down, or are coming down only slowly, or still going up in some markets (LOL?), because the last thing that landlords can afford to do right now, when they have to refinance a maturing mortgage, is to show that asking rents, if they can actually fill the space at those rents, will not support the new mortgage payments at the new interest rates.

Instead of lowering asking rents, landlords throw in massive concessions, from long periods of free rent, to fancy buildouts. And actual rents signed into the lease may also be lower than asking rents. And when landlords get tired of messing with it, they throw in the towel, give up on their investment, and walk away to let the lenders mess with it.

Massive reprising underway. So for example, the plot thickens in Los Angeles, where the availability rate rose to a record 27.6%. Last year, Canadian real-estate giant Brookfield defaulted on $1.1 billion in mortgages backed by office towers, and it is now getting rid of those towers.

In late March, it was reported that Brookfield made a deal to sell the 1-million-square-foot tower at 777 S. Figueroa for about $145 million to Consus Asset Management in South Korea. The debt on the building amounts to $319 million, composed of a $269-million mortgage and a $50-million mezzanine loan. The sale price would amount to less than half the value of the debt. We would assume that Consus Asset Management will make some kind of deal with the lenders.

Brookfield’s Gas Company Tower, which is collateral for a $350-million mortgage and a $65 million mezzanine loan, and its EY Plaza, which backs a $275-million loan, are in court-appointed receiverships and face foreclosure sales.

Who is on the hook? For some office mortgages, banks are on the hook, including foreign banks. But lots of the loans that have spectacularly blown up were held by investors not banks, by holders of commercial mortgage-backed securities (CMBS), mortgage REITs, PE firms, life insurers, holders of collateralized loan obligations (CLOs), etc.

So the delinquency rate of office mortgages that have been securitized into CMBS rose to 6.6% in February, according to Trepp, which tracks CMBS. And we’re just one year into it, so this is just the beginning because it will take years to get…

Read More: Office CRE Mess Keeps Getting Worse, Massive Repricing Underway