MoMo Productions/DigitalVision via Getty Images

Introduction

This article covers the Schwab Fundamental U.S. Small Company Index ETF (NYSEARCA:FNDA) (the “Fund“), a passively managed exchange-traded fund (“ETF“) managed by Charles Schwab Investment Management, Inc. (the “Fund Sponsor“). Awarded three-stars from Morningstar, the Fund boasts a low expense ratio (0.25%) and above-average relative performance. Notably, the Fund does not stand out compared to my favorite small-cap ETF, the Pacer US Small Cap Cash Cows 100 ETF (CALF) (“CALF“), although it does match up well with the Vanguard Small-Cap Growth Index Fund ETF (VBK) (“VBK“) (another small-cap ETF that I own).

Overall, while the Fund is solid, and I deem it a BUY, CALF, which I would consider a STRONG BUY, is likely a better option for investors seeking small-cap exposure.

Why Small Caps?

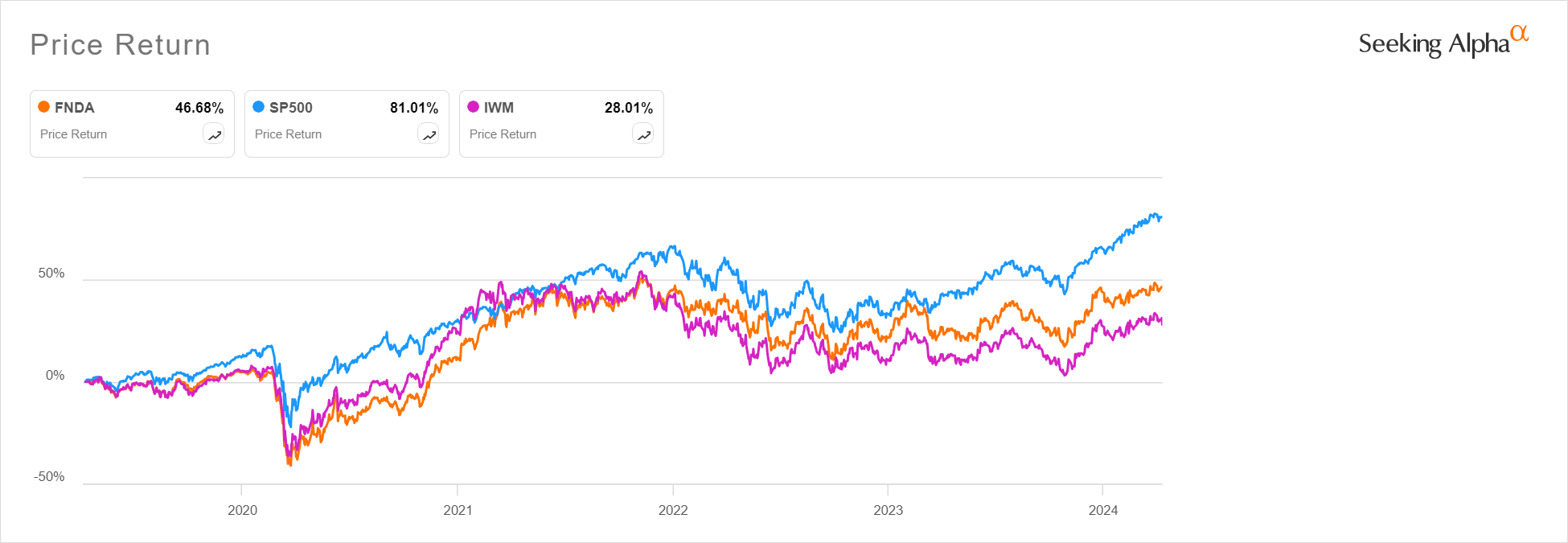

While I have been slowly increasing my portfolio’s allocation to small-cap stocks, I am still very underweight the category. Of course, small caps have been underperforming for several years, as is shown in the table below comparing the Fund, the S&P 500, and the Russell 2000 (using the iShares Russell 2000 ETF (IWM) (“IWM“) as a proxy for the Russell 2000) over a five-year period ending April 9, 2024.

5-Year Comparison (Seeking Alpha)

Valuation

Underperformance of small caps could mean opportunity, and the Fund has notably outperformed IWM over the five-year period. The table below shows that small caps historically trade at 6% discount to large cap stocks; however, at the beginning of 2024, that discount was above 30%.

Small Caps Trading at Discount (Voya Investment Management)

Source: Voya Investment Management

Moreover, according to Morningstar, key valuation metrics of the Fund compared to the S&P 500 (as expressed by the ticker SPY, the SPDR S&P 500 Trust) and CALF are shown below (as of April 11, 2024).

| The Fund | SPY | CALF | |

| Price to Book | 1.54 | 4.15 | 1.66 |

| Price to Sales | 0.93 | 2.70 | 0.61 |

| Price to Cash Flow | 7.09 | 15.0 | 4.70 |

| Price to Earnings | 15.47 | 21.87 | 12.05 |

The data clearly show that the Fund is much cheaper than S&P 500, and this valuation discount will have to narrow over time in my view (unless capitalism is broken). Notably, on three of the four valuation metrics, CALF is even cheaper than the Fund.

Given how cheap small caps are relative to large caps, I have acquired several small-cap positions, and have moved some money in my retirement accounts to a small-cap growth mutual fund.

I have continued to research small cap exchange-traded funds (“ETFs“), looking to diversify into a few different investments. In this regard, I have recently been looking at the Fund, which has successfully garnered more than $8 billion in assets since its August 15, 2013 inception date.

The Fund

Per its Prospectus, the Fund generally invests in stocks that are included in the Russell RAFI US Small Company Index (the “Index“). Specifically, the Prospectus provides that:

The Index selects, ranks, and weights securities by fundamental measures of company size – adjusted sales, retained operating cash flow, and dividends plus buybacks – rather than market capitalization. The index measures the performance of the small company size segment by fundamental overall company scores (scores). . . . Securities are grouped in order of decreasing score and each company receives a weight based on its percentage of the total scores of the U.S. companies within the parent index. The index is comprised of the smallest U.S. companies by fundamental size. The bottom 12.5% of the companies by cumulative fundamental score are included in the index. The weights of the companies included in the index are determined annually and are implemented using a partial quarterly reconstitution methodology in which the index is split into four equalsegments and each segment is rebalanced on a rolling quarterly basis.”

The Index is crafted by the Frank Russell Company and Research Affiliates LLC. While the fund is a passive vehicle, the investment advisor does have some discretion. According to the Prospectus:

[W]hen the investment adviser believes it is in the best interest of the fund, such as to avoid purchasing odd-lots (i.e., purchasing less than the usual number of shares traded for a security), for tax considerations, or to address liquidity considerations with respect to a stock, the investment adviser may cause the fund’s weighting of a stock to be more or less than the index’s weighting of the stock. The fund may sell securities that arerepresented in the index in anticipation of their removal from theindex, or buy securities that are not yet represented in the index inanticipation of their addition to the index.”

Moreover, the Prospectus provides that the Fund is…

Read More: FNDA: A Solid Small-Cap ETF (NYSEARCA:FNDA)