BING-JHEN HONG

Strong Results But Pricing Headwinds Have Arrived

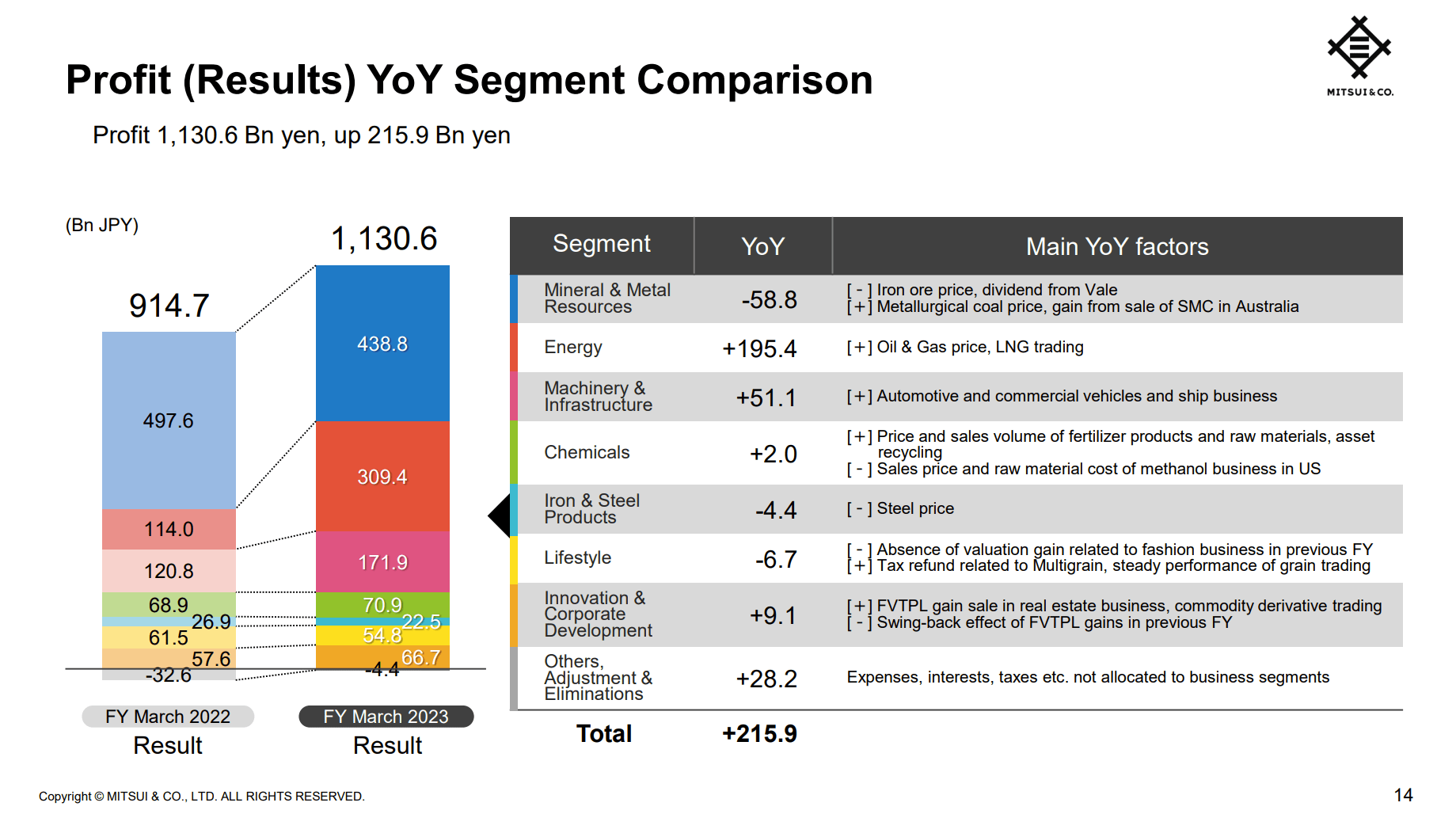

Mitsui & Co. (OTCPK:MITSF) (OTCPK:MITSY) delivered strong results in FY 2023 with a profit of ¥1130.6 billion, beating the last forecast of ¥1080 billion, which I discussed in my article last quarter. Also, the company declared a final dividend for the year of ¥75, an increase of ¥5 from the prior forecast. (The company’s fiscal year ends on March 31.) That brings the payout for the year to ¥140 per share. Strong oil, gas, and coal prices enabled the company to continue the string of regular beats and raises that characterized most of the last 3-year plan cycle. In FY 2023 in particular, energy prices were the big driver, offsetting declines in iron ore, Mitsui’s highest-volume metal business. Compared to FY 2022, the Energy segment increased its profit by 170%, more than offsetting lower results in the Metals & Minerals segment.

Outside of these basic materials, most of the other segments had steady results, except for Machinery & Infrastructure. This segment had some one-time gains on asset sales such as its stock in Lucid (LCID), but also strong results in the ship-related businesses, its stake in Penske Automotive (PAG) and Penske Truck Leasing, and other US Automotive businesses.

Mitsui & Co.

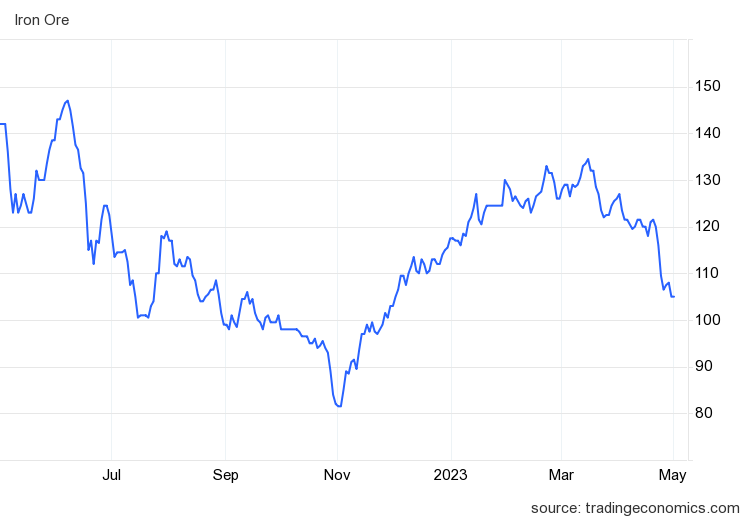

Looking forward, these commodity price headwinds appear to be strengthening. Mitsui does not disclose its iron ore price assumptions, but Trading Economics provides a grim outlook based on low demand from Chinese builders and steelmakers and higher supply from Australia.

Trading Economics

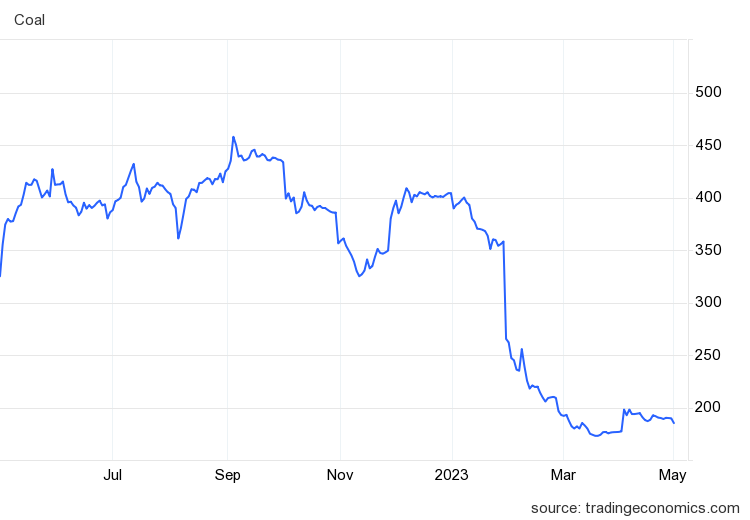

Coal prices have also fallen off a cliff to start the fiscal year.

Trading Economics

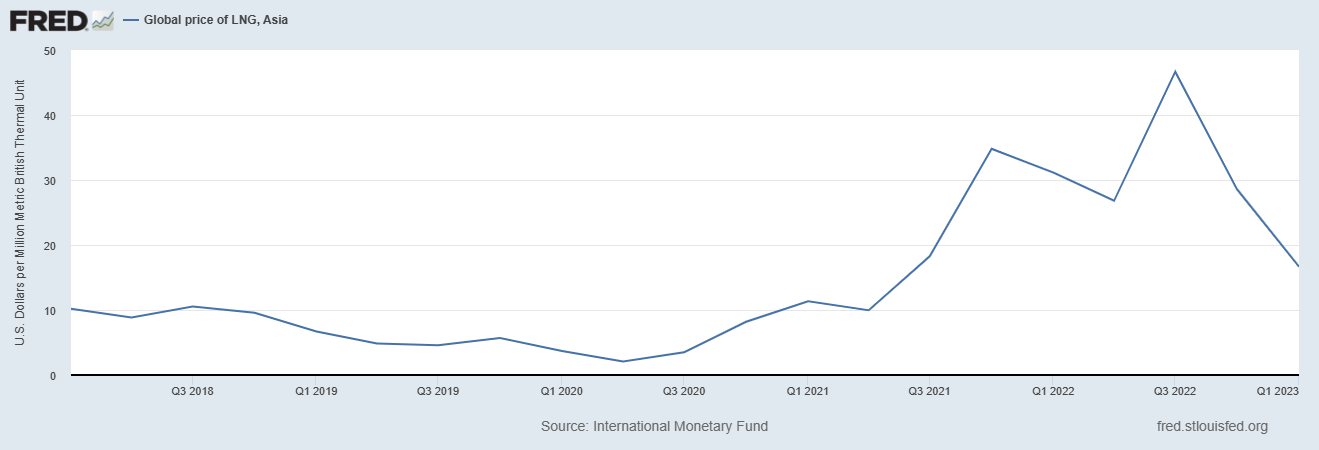

Commodities where Mitsui does disclose the forecast are also lower in FY 2024. The Japanese crude oil marker price assumption is $79/bbl, down from $103 last year. The Henry Hub gas assumption is $2.99/MMBtu, down from $6.51 last year. Asian LNG prices, more directly applicable to Mitsui, are also down after a spike last year.

St. Louis Federal Reserve

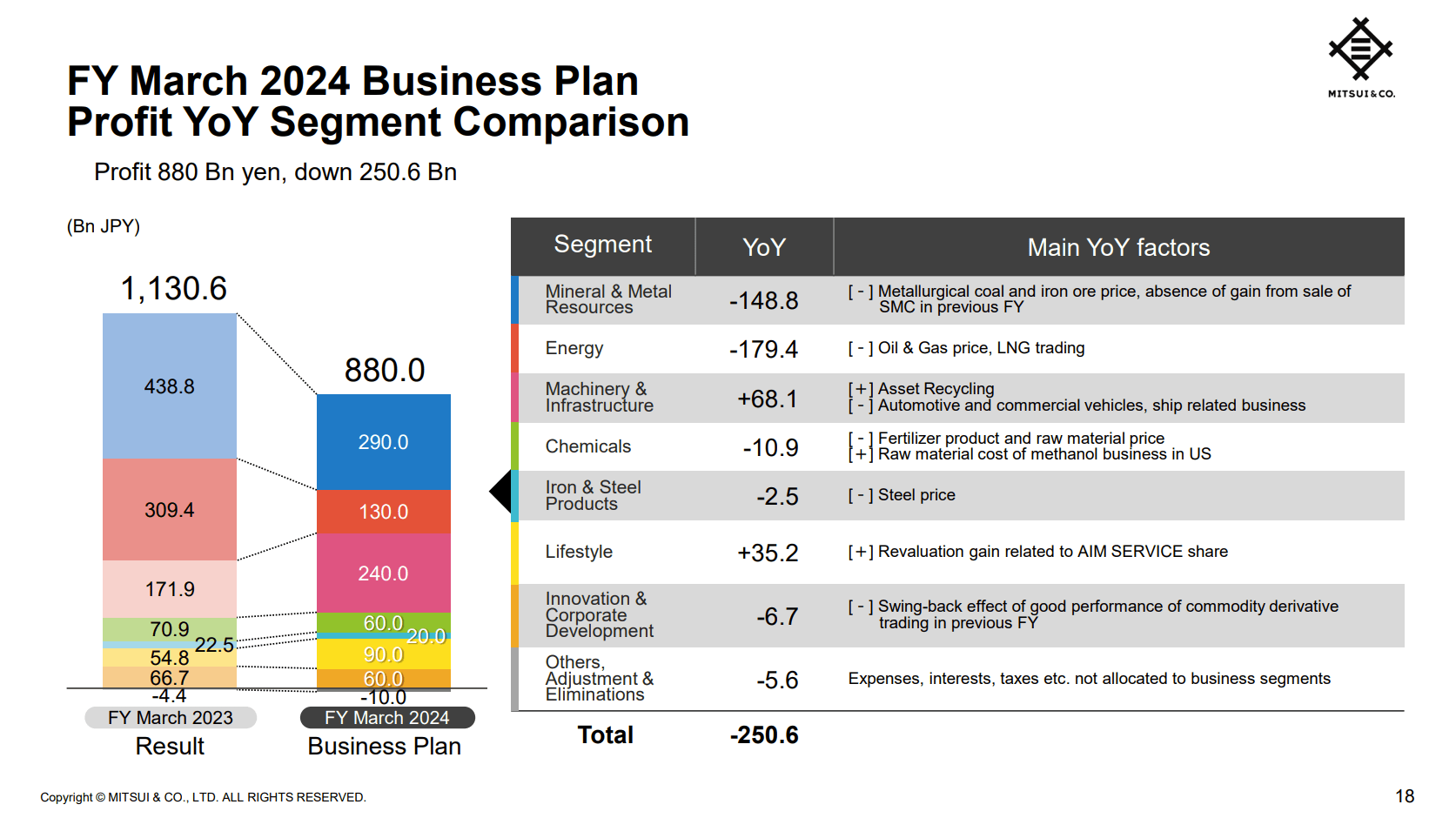

Given these price declines, Mitsui’s initial forecast of FY 2024 profit is ¥880 billion, down 22% from FY 2023 actuals. The two commodity-based segments comprise less than half of Mitsui’s planned profits in FY 2024.

Mitsui & Co.

As we see from the forecasted profit decline, Mitsui remains a deeply cyclical company. However, the company is working to get back to the trillion-yen annual profit level without having to rely on unusually high commodity prices, which we will see in their new 3-year plan.

3-Year Plan: Solid Growth Once You Sort Through The ESG Hype

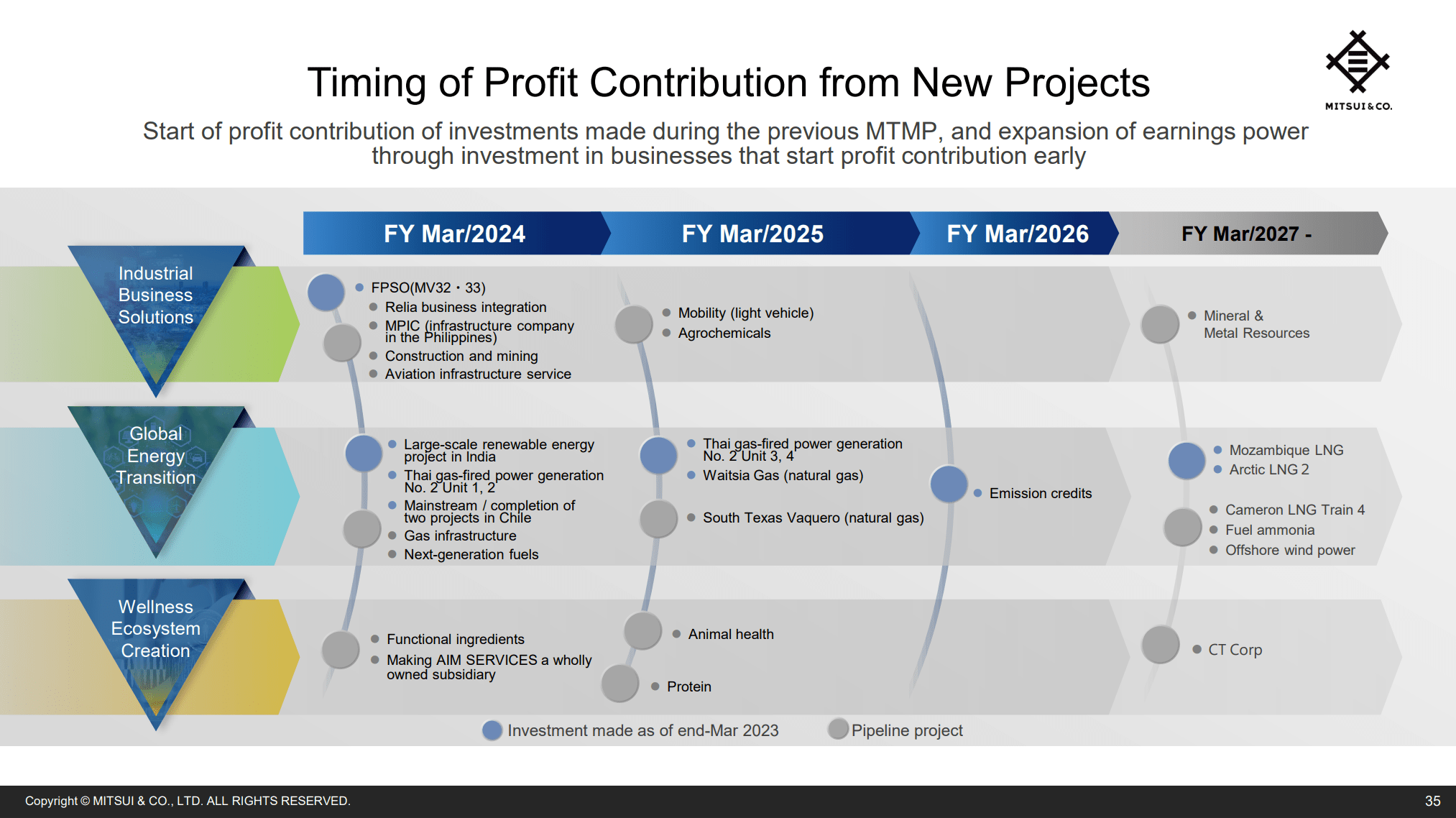

FY 2024 marks the start of a new 3-year Medium-Term Management Plan period for Mitsui. The theme switches from “Transform and Grow” in the last plan to “Creating Sustainable Futures” in the new one. It appears no corner of the world is immune from ESG buzzwords, and this new plan is full of gems like “Deeper sustainability management”, “Strengthening of group management capability”, and “Promotion of globally diverse individuals”. The important parts of the plan, however are the three strategic initiatives where Mitsui will actually direct investment over the plan period. These are Industrial Business Solutions, Global Energy Transition, and Wellness Ecosystem Creation.

When we dig into the details, we see that the strategic initiatives are extensions of Mitsui’s existing business and not an abrupt switch to green projects for their own sake. Industrial Business Solutions includes investments in a business process outsourcing company, infrastructure development in the Philippines, and extending the company’s involvement in transportation worldwide. Global Energy Transition does indeed include some renewable energy businesses and a carbon credit trading company, but the bulk of new investments are in LNG and gas-fired power generation. The Wellness Ecosystem covers the entire food chain from agricultural chemicals and commodities to food service companies like Aim Services to healthcare businesses like pharmaceuticals and hospital operations.

Mitsui & Co.

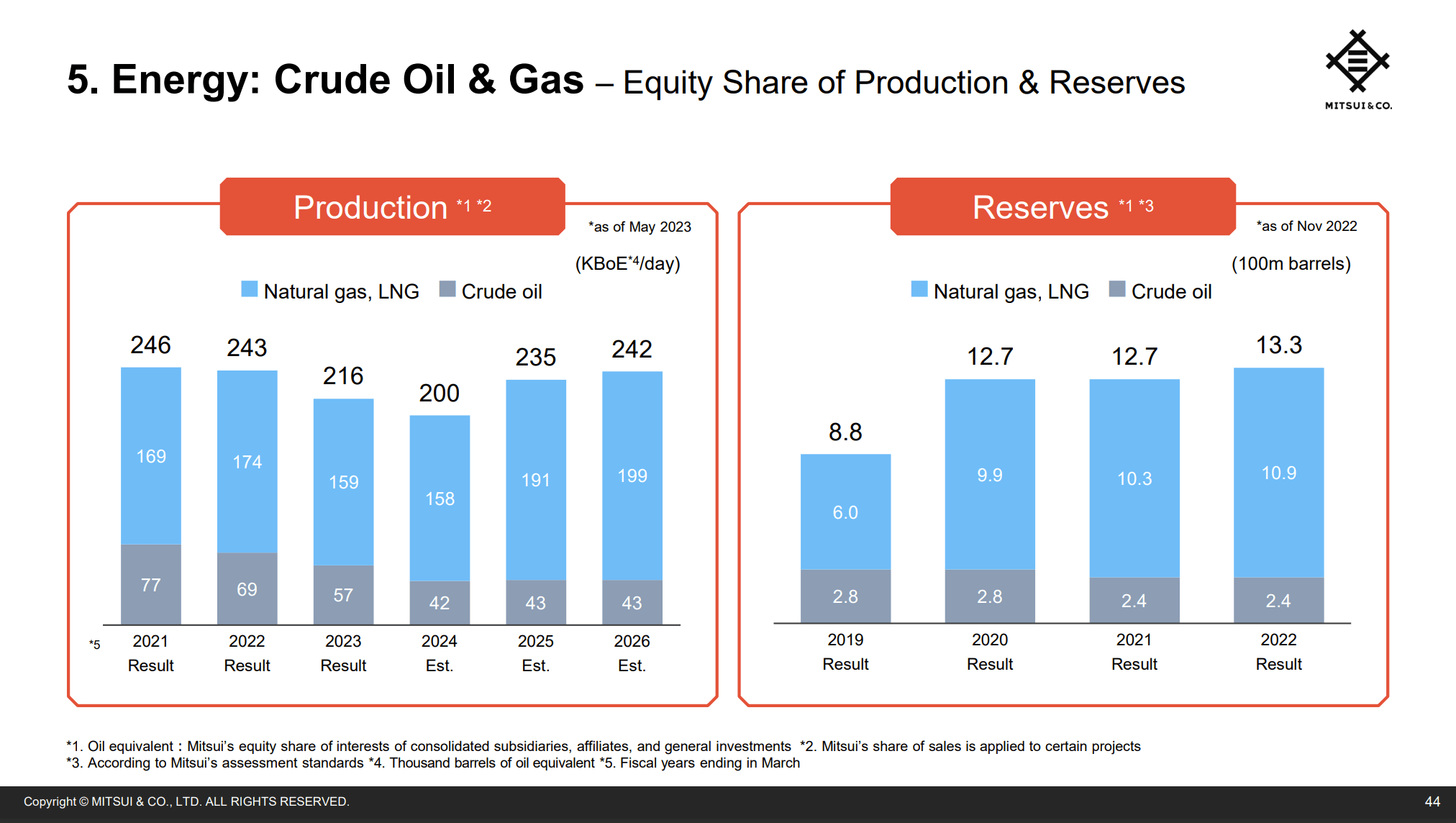

As another sign Mitsui is not straying too far from its core businesses, we see recovery of volumes in the Energy segment over the plan period with focus on LNG.

Mitsui & Co.

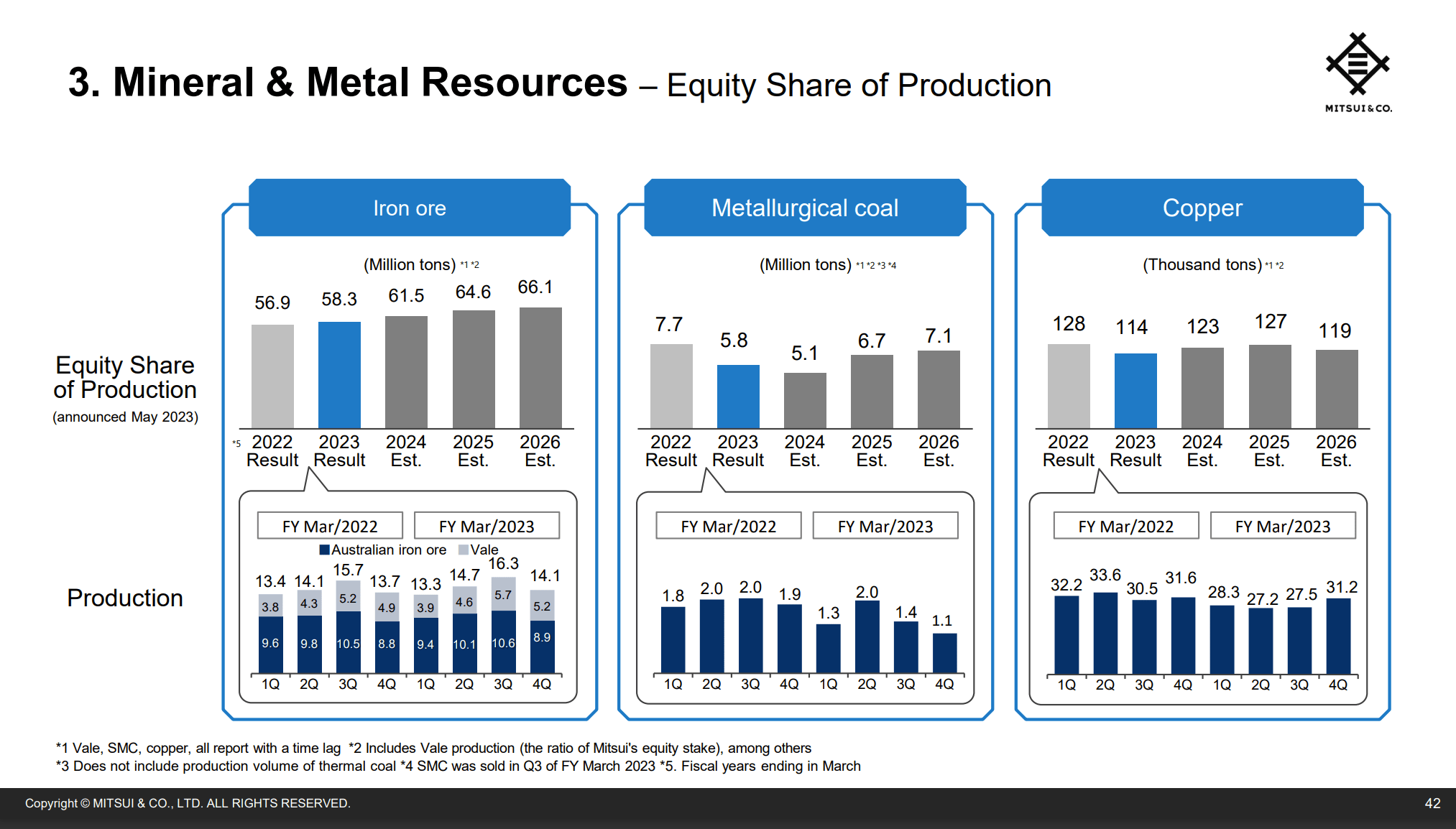

Within Metals & Minerals, we see growth in iron ore and recovery of met coal volumes following the sale of 1.2 million tonnes of coal capacity in Australia last year.

Mitsui & Co.

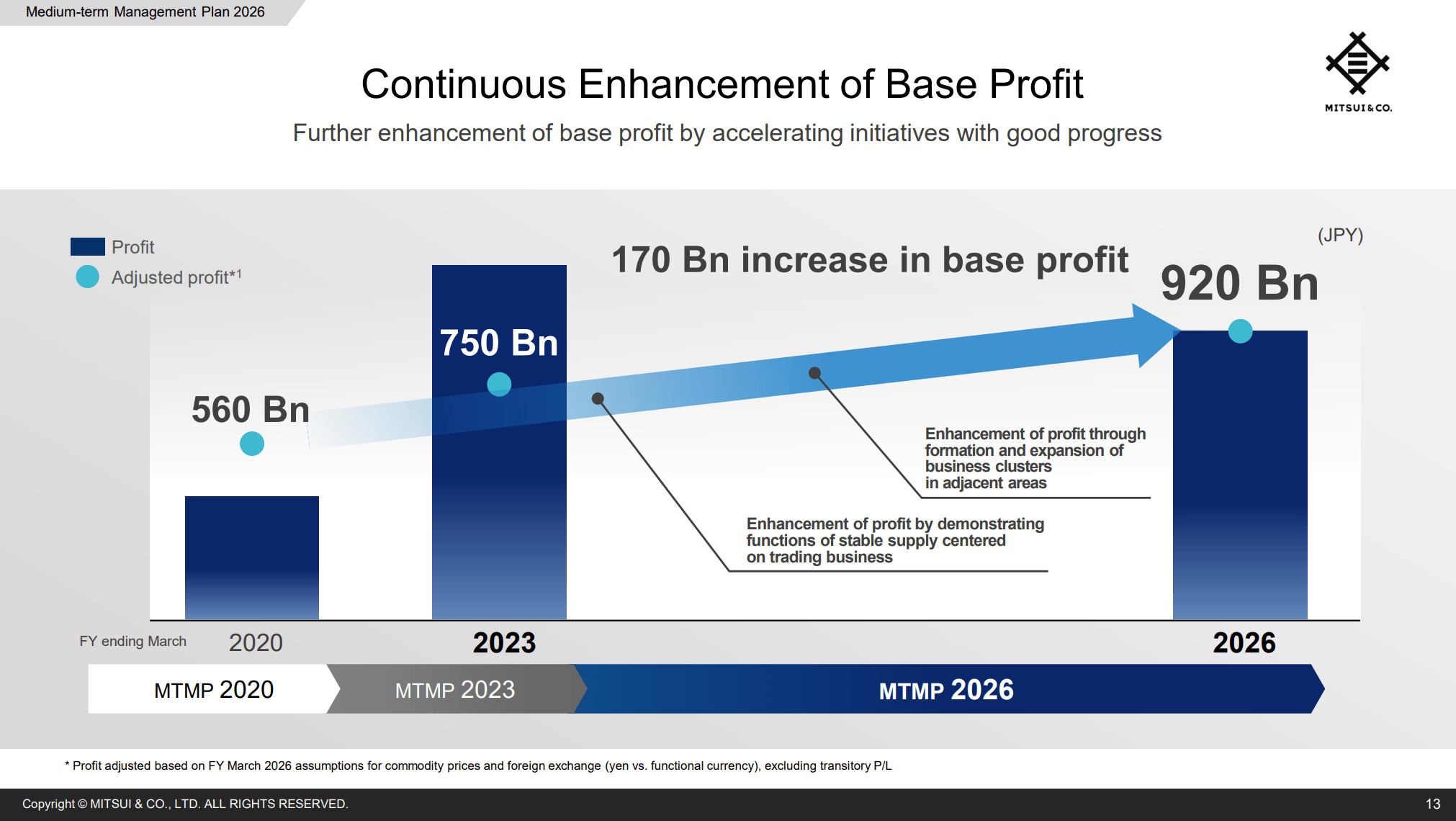

The financial result of this plan is that Mitsui expects to increase earnings power in a mid-cycle commodity price environment ¥170 billion by FY 2026 to ¥920 billion profit, and around ¥1 trillion in free cash flow. While these results are not much different from 2023 actuals, they do not rely on high commodity prices to achieve.

Mitsui & Co.

Valuation And Capital…

Read More: Mitsui Stock: Solid Conglomerate With Cyclical Headwinds (MITSF)