Dazman/E+ via Getty Images

We’re more than halfway through the Q1 Earnings Season for the Gold Miners Index (GDX) and one of the most recent companies to report its results is SSR Mining (NASDAQ:SSRM). From a headline standpoint, the company’s numbers certainly weren’t pretty, with ~146,900 gold-equivalent ounces [GEOs] produced at all-in sustaining costs of $1,693/oz and revenue down 11% year-over-year despite stronger metals prices. However, Q1 was an abnormally weak quarter due to much lower production at Seabee and Çöpler and sustaining capital being front-end weighted, translating to ugly Q1-23 results. Let’s take a closer look at the results below.

SSR Mining Operations – Çöpler (Company Website)

Q1 Production & Sales

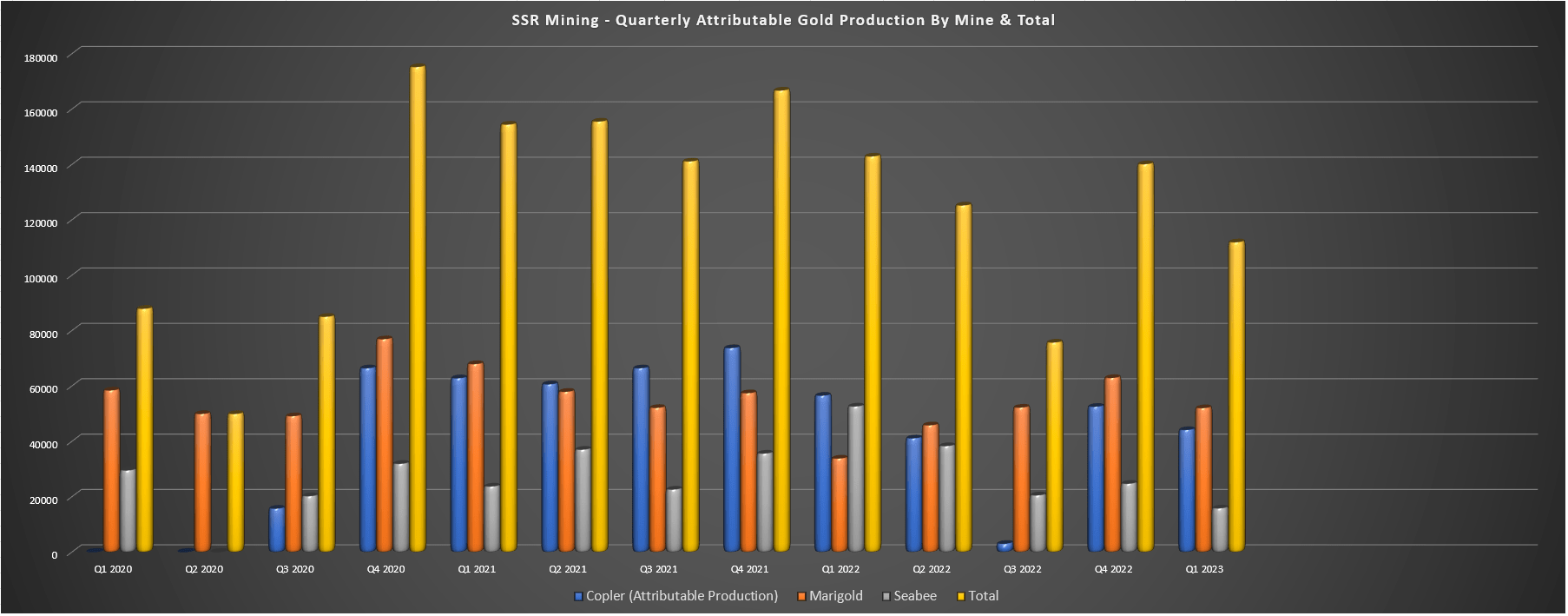

SSR Mining released its Q1 results last week, reporting quarterly production of ~146,900 GEOs, a 15% decline from the year-ago period (Q1 2022: ~173,700 GEOs). The sharp decline in output was related to lower sulfide grades at Çöpler that was only partially offset by higher oxide grades, and a significant decline in production at Seabee, which saw equipment downtime in Q1 and was up against difficult comps after enjoying grades above 17.0 grams per tonne of gold in Q1 2022. And while Marigold and Puna had better quarters with ~52,000 ounces of gold produced and ~28,400 GEOs produced, respectively, this wasn’t able to offset the tough comps at its two higher-margin assets.

SSR Mining – Quarterly Attributable Production by Mine & Total (Company Filings, Author’s Chart)

Beginning with its flagship asset, Çöpler, the asset produced just ~55,100 ounces of gold (100% basis) in the quarter, down over 21% from the ~70,600 ounces of gold produced in the year-ago period. As noted above, while oxide grades were up year-over-year with significantly more tonnes stacked (~188,000 tonnes at 1.22 grams per tonne of gold), sulfide grades were down sharply and the higher throughput of ~724,000 tonnes and slightly higher recoveries still translated to materially lower production year-over-year. The result was that all-in sustaining costs soared to $1,420/oz from $955/oz in the year-ago period, providing little help to what would already be a high-cost quarter.

Marigold Operations (Company Presentation)

Moving over to the much lower-grade Marigold Mine in Nevada, production was up significantly year-over-year to ~52,000 ounces, but this was due to easy year-over-year comps (Q1 2022: ~37,000 ounces produced). The increase in production was driven by higher tonnes stacked and a slightly higher average gold grade, with ~5.37 million tonnes stacked in Q1 at an average grade of 0.42 grams per tonne gold. SSR Mining noted in its prepared remarks it expects to recover the remainder of the material stacked last year with a slower turnaround in Q2, and also confirmed that it’s stacked more competent ore this year with investors able to expect more normal leach cycles, which should translate to more predictability in terms of ounces recovered.

Unfortunately, the significant increase in production did not translate to lower unit costs, with Marigold’s AISC increasing nearly 6% year-over-year to $1,663/oz. However, it’s important to note that cash costs were relatively flat at $1,066/oz and the increase in AISC was related to significant sustaining capital in the period related to haul truck purchases, with Q1 sustaining capital of ~$29.0 million coming in at ~36% of the annual guidance range. Hence, there’s no reason to believe that Marigold can’t meet its cost guidance of $1,315/oz to $1,365/oz despite the slow start to 2023, and while cyanide costs continue to be pressured, the company is getting some help from lower fuel prices and a weaker United States Dollar.

Seabee Mine – Saskatchewan (Google Earth)

Finally, looking at SSR Mining’s smallest gold operation, Seabee, the mine produced just ~15,800 ounces in Q1 2023, a significant decline from ~52,600 ounces in Q1 2022. While this is an alarming drop on a year-over-year basis, Seabee had to lap an unusually strong quarter where it benefited from head grades of 17.7 grams per tonne of gold. And the mine unfortunately saw equipment downtime in Q1 that shifted the mining sequence, making for a far worse quarter than planned. That said, SSR Mining expects Seabee’s grades to improve materially as the year progresses, with AISC set to improve from the $2,207/oz reported in Q1 with lower sustaining capital and higher volumes.

Costs & Margins

Moving over to costs and margins, SSR Mining’s consolidated AISC came in at $1,639/oz in Q1, a 55% increase from year-ago levels. The higher costs were related to fewer ounces sold and a significant increase in sustaining capital, which soared from $38.7 million to $51.7 million, placing a dent in margins in the…

Read More: SSR Mining Stock: Ignore The Weak Q1 Results (NASDAQ:SSRM)