grandriver

Investment thesis: The EIA came out with a notable forecast that the market and the MSM hardly noticed, even though the potential impact on the global oil (CL1:COM) market and the global economy perhaps as early as this year could be dramatic. The EIA forecast calls for near-stagnated US crude oil output for this year and next, which does not seem all that dramatic until we add historical context. The context I am referring to is the fact that for the past decade and a half US shale and to a lesser extent Canadian oil sands provided most of the global crude oil supply growth, with shale playing an outsized role.

With US crude oil production set to stagnate this year, while global demand is forecast to grow, a severe tightening of the global supply/demand situation is set to occur, so we could see potentially significant shortfalls in supply. The investment implications can be assumed to include lower company revenues & profits, even as expected rate cuts will fail to materialize, meaning that markets are likely to end the year much lower compared with where we started the year.

The EIA report:

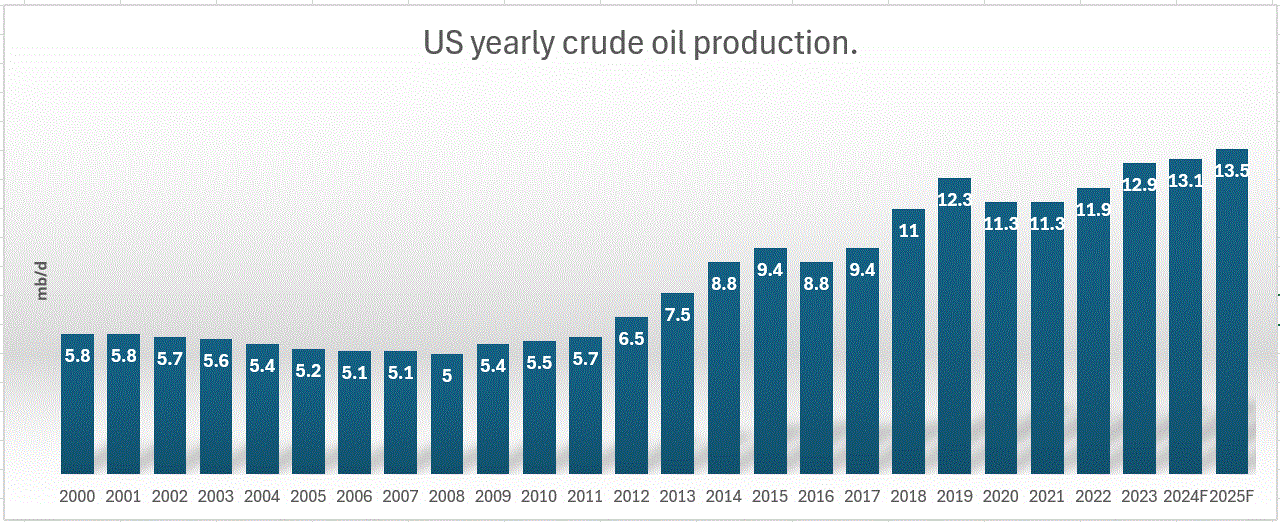

For 2024, the EIA forecast for yearly US production suggests that we are still in expansion mode, albeit at a much slower rate of increase. At first glance, there seems to be nothing particularly newsworthy about this report.

Data source: EIA

The detail that makes this report significant is that for the past few months, the EIA has been reporting daily US crude oil production volumes of about 13.3 mb/d, in other words, higher than the expected average for this year. This means that the US is expected to see a decline in production when looking at monthly data instead of yearly average production rates.

It should be noted that the EIA does provide a silver lining in its forecast in the form of an assumed increase in production in 2025 that is somewhat higher in yearly terms compared with this year. It is unclear what will trigger a reversal of a forecast decline this year in monthly terms. For 2024 the EIA had access to metrics such as expected capital spending at the company level for the industry, which provides a decent indication regarding where production might be headed. The same cannot be said for 2025 because even if companies provide some indications of their longer-term plans, those numbers are only preliminary. Even if the EIA forecast for both years turns out to be correct, it will mean an annual average production increase that is much lower compared with previous years and only a marginal increase compared with recent monthly production averages.

What the world economy would have looked like in the past decade and a half without US shale & Canadian oil sands

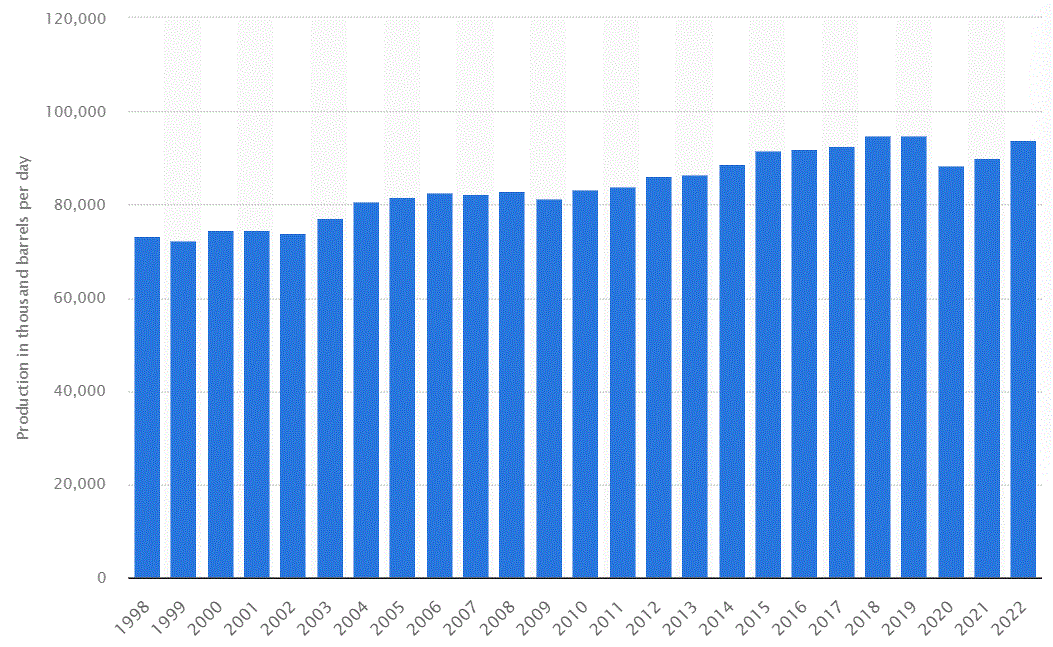

The contribution the US shale boom provided to global energy stability since 2008, cannot be overstated. It provided an extra 8 mb/d to the global supply tally. Together with Canada, which also saw an increase in production, the two countries account for about 75% of all global oil supply growth over the decade-and-a-half period.

Global oil production (Statista)

Without the shale boom and growth in Canadian oil sands production, global crude oil production would have grown by only about 3 mb/d in the 2008-2022 period. In other words, the world would have experienced a permanent oil price crisis, punctuated only by demand destruction events.

My back-of-the-envelope formula for the global GDP growth/oil supply relationship, which I have been using for many years now, looks as follows:

1.5% efficiency growth/year + (Oil supply % growth x 2) = Maximum potential global GDP growth/year.

Total yearly global oil supply growth averaged about 1% for the 2008-2023 period. Looking at the average yearly global GDP growth for the period, it was around the 3% mark, which pretty much fits my formula. I should note that I am not using this formula as a reference for shorter-term economic growth prospects, but rather for longer-term, multi-year average potential growth.

If we were to assume that without shale & oil sands global oil supply growth would have been only about .4%, the maximum average GDP growth/year would have been about 2.3%, without accounting for systemic secondary effects.

What the future might look like in the stagnated shale production scenario

- Efficiency gains to provide the only source of economic growth if global oil production stagnates.

The fact that the growth of conventional global oil supply stalled out in the past decade and a half suggests that we most likely reached the maximum level of global production capacity. Unconventional resources, mostly US shale, and to a lesser extent Canadian oil sands filled the gap, but it seems we reached the limits of this trend as well. Assuming that global oil production is set to more or less…

Read More: Shale Stagnation Expected After Previously Underpinning Global Supply Growth