NanoStockk/iStock via Getty Images

We are going to cover, in detail, what the differences are between monetary policy and fiscal policy – in practical terms – and what this means for investors in 2024 and beyond. Then to pay back that investment of mental time and energy, we will discuss the Net Liquidity model and how and why it correlates particularly well with the stock market.

In Part 1 we focused on the Yield Curve and why a more detailed reading of the measure is required to understand how this measure can be used for forecasting. In Part 2 I argued that we should be taking a contrarian approach to modern recession forecasting and ignore a great deal of the mainstream media, including the NBER dating committee. We then focused on helpful indicators like Heavy Truck Sales and the FSI index in Part 3.

In this piece we want to both build our knowledge of how the financial system works, and to understand what Liquidity is and how it can help us to make sense of the multitude of fiscal programmes that are out there while giving a sense of the impact they have on the stock market.

An ambitious set of targets – let us get started!

Policy – Two Big Levers

One of the biggest concepts that investors misunderstand is the fact that there is not simply one individual component or metric that can be focused on in isolation. The market is much more efficient now than it was in the past: which means you need multi-factor models and greater depth of understanding to have an edge. Basic moving averages and technical analysis alone are not enough. The financial system, and in particular fiscal policy, fits together as part of a large and broad house that works together.

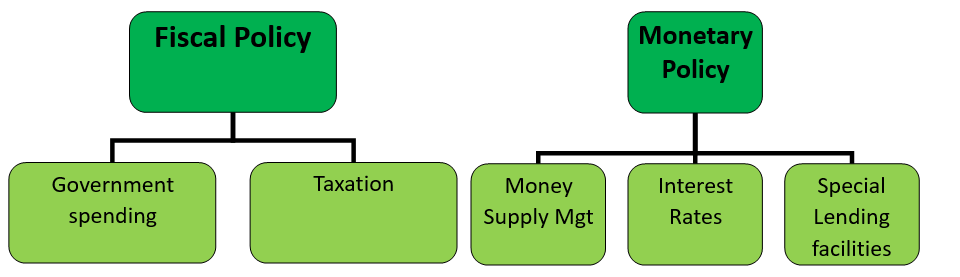

Starting with basic features of that house – there is Fiscal policy and Monetary policy. These are the tools that the government and central banks use to influence the economy in significant ways.

Let’s use a chart to illustrate the differences between the two:

David Huston – Policy

Imagine these levers may be pushed forwards (stimulative) and backwards (reducing aggregate demand).

It is fiscal policy that is really in the driving seat. Money drives the market and I intend to go through what monetary policy is, then end with what fiscal policy is and show that it is significantly more predictive for asset prices and the stock market.

Monetary Policy

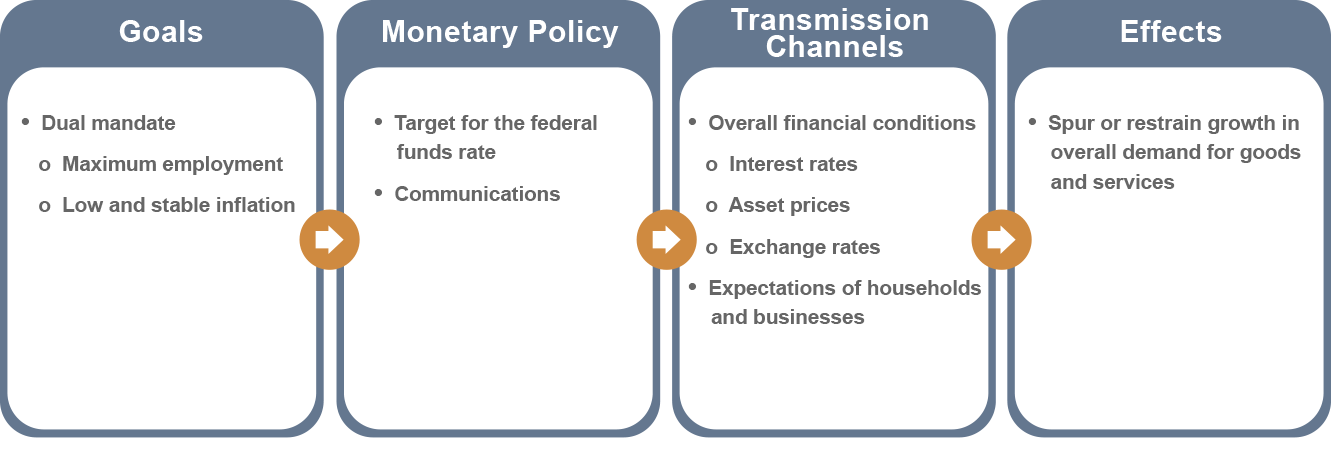

Starting with Monetary Policy. I suspect that investors have had a crash course in monetary policy recently. The aim of said policy is to achieve objectives that are set out in the Federal Reserve’s mandate as the central bank. That mandate is defined by the Federal Reserve Act:

The Federal Reserve Act mandates that the Federal Reserve conduct monetary policy ‘so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.’1 Even though the act lists three distinct goals of monetary policy, the Fed’s mandate for monetary policy is commonly known as the dual mandate.

The reason is that an economy in which people who want to work either have a job or are likely to find one fairly quickly and in which the price level (meaning a broad measure of the price of goods and services purchased by consumers) is stable creates the conditions needed for interest rates to settle at moderate levels.2”

Source:

Frederic S. Mishkin (2007), “Monetary Policy and the Dual Mandate,” speech delivered at Bridgewater College, Bridgewater, Va., April 10

They enshrine their goals and the instruments or “transmission channels” that they use to achieve those goals very clearly in Mishkin’s paper, and I include an extract here:

Mishkin 2007 Monetary Policy speech

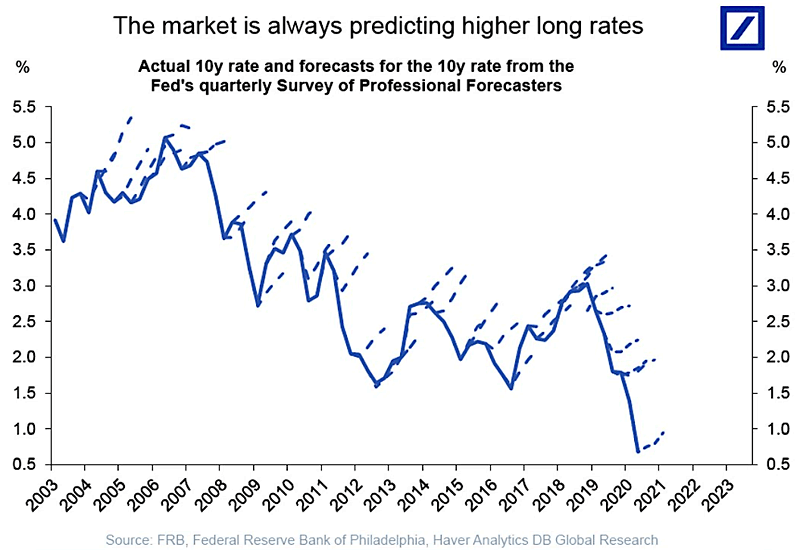

As we have discovered in 2022-2023, though; there is an inordinate amount of attention given to monetary policy. Millions of investors tune into Powell’s speeches and eagerly await any nuggets of wisdom that they can get regarding the future direction of policy. When will they start cutting rates? Can anybody trick Powell, through crafty questions, into revealing when the first interest rate cut will be?

What fascinates me about this is that it is so futile. Monetary policy forecasts – by the Fed, by independent economists, by hedge funds and banks – all tend to be wrong and certainly no better than a coin flip. The direction of monetary policy does not fundamentally drive the stock market – meaning, it’s not as strong a lever as investors tend to believe because you can’t easily act on it to make money.

As Haver Analytics and the Federal Reserve Bank itself points out, forecasts are (nearly) always wrong and often too high:

Haver Analytics DB Global Research 2021

Despite what you may read in the news, for most modern history in the US stock market, there was simply no sustained correlation…

Read More: Recession Forecasting: Fiscal Policy And Liquidity Drive Stock Market Direction