PM Images

The PIMCO Corporate & Income Strategy Fund (NYSE:PCN) is a closed-end fund, or CEF, that investors can use to earn a very high level of income. The fund’s 9.83% yield indicates that it should do a reasonable job at this, although the yield is quite a bit lower than many other PIMCO closed-end funds. This may not be a bad thing though, since any time a fund’s distribution gets above 10% or so, it is a sign that the market expects that it may have to cut its distribution in the near future. The PIMCO Corporate & Income Strategy Fund has not hit this level yet, so that could be a very good sign.

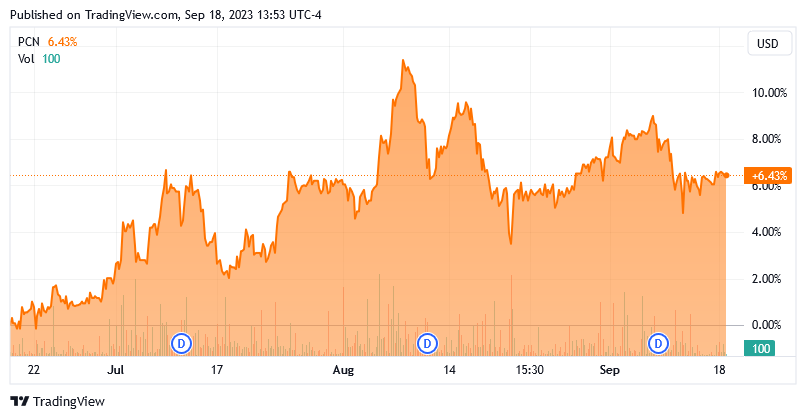

The fund has been performing very well in the market lately, as it is up 6.43% in the past three months:

Seeking Alpha

These recent gains may or may not be sustainable though, as there are currently numerous reasons to believe that the market is being far too optimistic on bonds and interest rates. After all, inflation has started to tick up as oil prices recently passed $90 per barrel, which is the highest level that they have had since November 2022. In addition, the core consumer price index remains at close to double the Federal Reserve’s target level. These things could cause the Federal Reserve to raise interest rates, rather than cut them as the market expects. This could very quickly cause this fund to erase all of the gains that it has enjoyed over the past few months. When we combine this with the fact that the fund’s shares appear to be substantially overvalued relative to their intrinsic value, it may be best to sit on the sidelines for the time being.

As regular readers may recall, we last discussed this fund back in July. While many of the comments that I made in that article about this fund are still valid, there have been some events since that time that have made the bond market riskier than it was previously. This extends to this fund, so it is worth revisiting this fund to determine if it really is worth the potential risks.

About The Fund

According to the fund’s webpage, the PIMCO Corporate & Income Strategy Fund has the objective of providing its investors with a high level of current income. This is a very common and understandable objective for a bond fund. This one includes much more than this in its description of its strategy and objectives, however. From the webpage:

Using a dynamic asset allocation strategy that focuses on duration management, credit quality analysis, risk management techniques, and broad diversification among issuers, industries, and sectors, the multi-sector fund seeks high current income, with a secondary objective of capital preservation and appreciation.

Under normal market conditions, the Fund seeks to achieve its investment objective by investing at least 80% of its net assets plus borrowings for investment purposes in a combination of corporate debt obligations of varying maturities, other corporate income-producing securities, and income-producing securities of non-corporate issuers, such as U.S. Government securities, municipal securities and mortgage-backed and other asset-backed securities on a public or private basis.

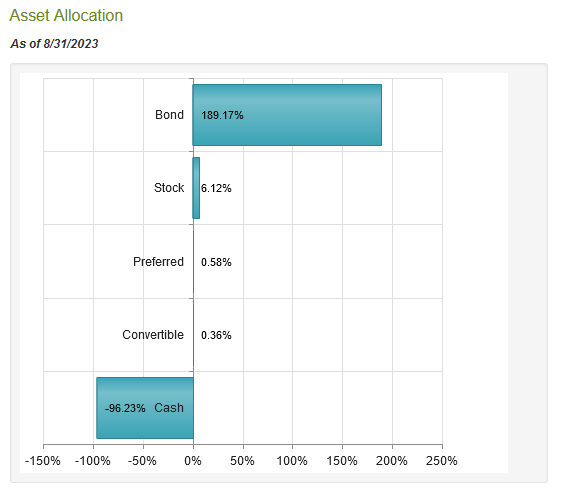

This description strongly suggests that the PIMCO Corporate & Income Strategy Fund is a fixed-income fund, which is exactly what we would expect from PIMCO. After all, PIMCO is quite well known as being a bond house. The fund’s asset allocation supports this conclusion. As of the time of writing, the fund has 189.17% of its assets invested in bonds, alongside comparatively small allocations to both common and preferred stocks:

CEF Connect

One immediate question that someone looking at the above table might ask is how the fund can have a negative allocation to cash. This comes from the fact that this fund employs leverage as a way to improve its returns. We will discuss this later in this article, but for now, it is important to keep in mind that this boosts both the fund’s total returns and potential losses relative to a fund that is not employing leverage.

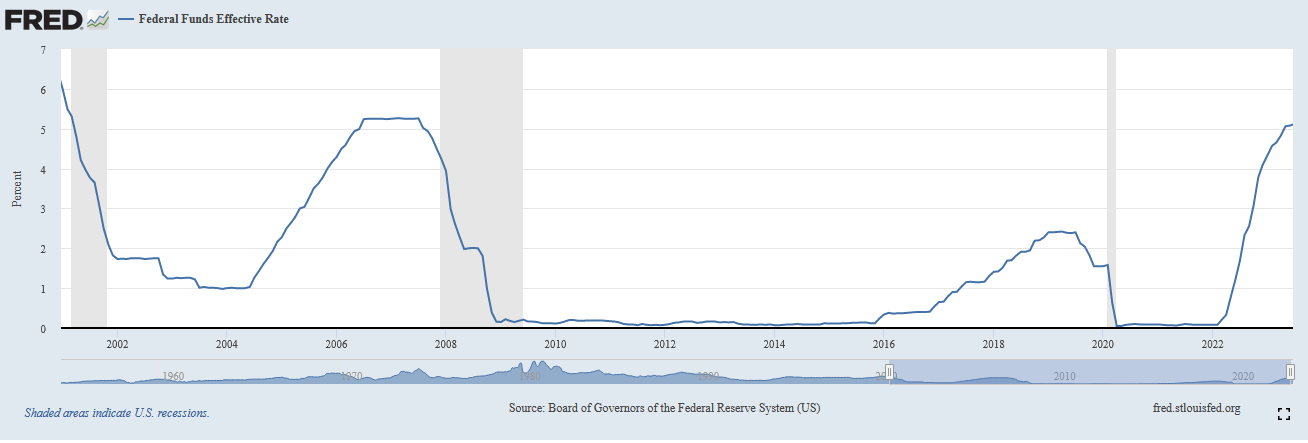

One of the defining characteristics of bonds is that their price declines when interest rates rise. This is one reason why the fund’s recent performance makes no sense. After all, the Federal Reserve has been very aggressively raising interest rates since the early months of 2022 in an attempt to combat the incredibly high rate of inflation that is pervasive in the economy. As of the time of writing, the effective federal funds rate is at 5.33%, which is the highest level that has been seen since early 2001:

Federal Reserve Bank of St. Louis

For those that can remember it, the early months of 2001 were around the time that the Internet bubble burst, and it goes without saying that this was a much stronger economy than we have today. Indeed, that was arguably…

Read More: PCN: Great Bond Fund, But Enormous Premium Presents Risks