Ronald Martinez

Investment thesis

The Energy Information Administration reports a robust performance in U.S. oil production, reaching a record 13.13 million barrels per day in 3Q 2023, exceeding earlier forecasts. The outlook for subsequent quarters indicates a continued upward trend, with plans to increase production to 13.31 mbd by 4Q 2024. This positive trajectory suggests a favorable operating environment for oilfield service companies.

Although the U.S. rig count is below pre-COVID-19 levels, the expected average rig count is 892 in 2023 versus the old forecast of 889 and 845 in 2024 versus the old forecast of 1,000. The decline in the forecast rig count is expected to be offset by higher well productivity, reinforcing the positive outlook for oil production.

We have not changed our view of the company since our previous analysis of the financial results for the second quarter of 2023, and in this report, we present the adjustments we have made to our forecast, in particular taking into account changes in the forecast for oil prices and oil production volumes in the United States. The company reported in Q3 2023 according to our expectations, the forecast logic has been maintained. Having in mind high oil prices in the foreseeable future, Halliburton is uniquely positioned to deliver financial outperformance. Rating is BUY.

Oil market balance and Brent prices

Supply

In light of voluntary production cuts in Saudi Arabia (by 1 mbd in July-December) and Russia (by 0.5 mbd in August and by 0.3 mbd in September-December, all from the June levels), we expect oil market shortages to persist through the end of the year. That will lead to higher oil prices, despite weak demand in the EU and the US.

The hurricane season in the Gulf of Mexico lasts from June through November, with its most active phase falling in August-October. Heavy storms can push oil production in the Gulf (about 17% of total US production) down by 0.5-1 mbd for 1-2 weeks. Hurricanes can cause short-term hikes in oil prices.

Amid the easing of US sanctions, we expect Venezuela to steadily ramp up oil output by 0.25 mbd, from 0.7 mbd in September of 2023 to 1.0 mbd in 1Q 2024.

Demand

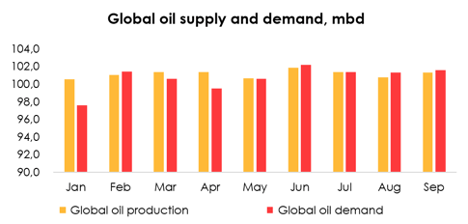

China’s oil demand climbed from 15.35 mbd in August to 16.14 mbd in September (+0.8 mbd). Seasonally, oil consumption in this country grows in September relative to August (by 0.7-0.9 mbd), and in December relative to September (by 0.4-0.6 mbd). At the same time, Chinese oil demand may be weaker in October (staying at the August level) due to seasonal maintenance at Asian refineries. We expect China’s oil demand to rise to 16.7 mbd in December 2023 on the back of economic development and seasonality.

Our assessment is that the EU is going through an economic downturn that’s close to a recession. EU oil demand fell from 13.9 mbd In July to 13.8 mbd in August. We anticipate that the demand will decline to 13.65 mbd in September and continue to weaken through December 2023.

US oil demand dropped from 20.4 mbd in August to 19.8 mbd in September of 2023 (by 0.6 mbd). We expect US oil demand to decline on the back of a slowing economy to 19.6 mbd in October 2023 and continue to weaken until March 2024.

Invest Heroes

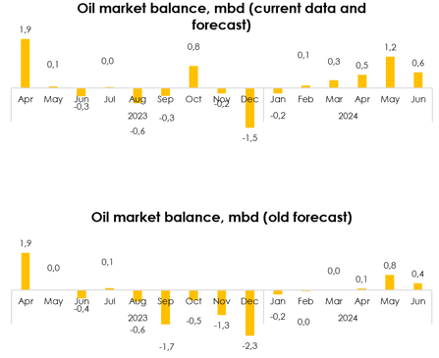

Based on the above reasons, we have changed our oil market balance forecast for October 2023 from a deficit to a surplus, compared to the one we described in the previous report. We expect oil to remain in short supply in November-December 2023 (due to the OPEC+ deal and voluntary oil production cuts), even as the EU economy is slowing and the US economy is expected to slow.

We anticipate the oil market will have a shortage of an average of 0.1 mbd in 1Q 2024. Our expectation is that in 1Q 2024 OPEC+ will not extend the voluntary production cuts, so OPEC output will be around 33.8 mbd (up from 32.9 mbd in September 2023). We expect oil supply to exceed demand in 2Q 2024 (on the back of rising non-OPEC production and seasonal weakening of demand in spring), providing the market with a surplus of an average of 0.8 mbd.

Invest Heroes

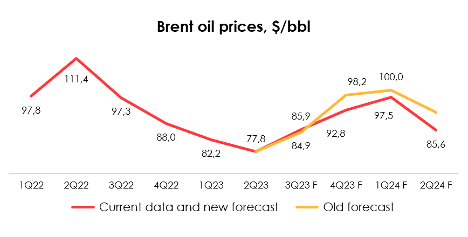

We have taken note of the higher-than-expected Brent price in September ($92.4/bbl versus the forecast of $89.5/bbl). We have also cut the forecast for the Brent price in October from $93.8/bbl to $88.5/bbl in connection with the change from a shortage to a surplus in the outlook for the oil market balance in October.

As such, we are lowering the forecast for the average Brent oil price in 2023 from $85.8/bbl to $84.7/bbl. We expect the price to go up from $85.9/bbl in 3Q 2023 to $92.8/bbl in 4Q 2023. We are lowering the oil price forecast from $100/bbl to $97.5/bbl for 1Q 2024, and anticipate the Brent price to slide to $85.6/bbl in 2Q 2024 amid a surplus in the market.

Invest Heroes

US oil production

We have covered this stock…

Read More: Halliburton: Buy Rating On Rising U.S. Oil Production (NYSE:HAL)