zhengzaishuru

Riding the energy boom in 2021 to late 2022, oil majors such as Exxon Mobil Corporation (NYSE:XOM) and Chevron (CVX) have accumulated record profits. Then, in early 2023 oil (CL1:COM) intermittently dropped to prices below $60/ barrel (WTI benchmark), down from $110/ barrel in 2022, and the oil bull market was considered to have ended. During the past few months, however, the oil bulls appear to have celebrated a stealth comeback: On the backdrop of stronger than expected economic activity, in combination with a hawkish OPEC, oil is slowly edging once again towards $100/ barrel. Like in the money markets, the mantra “higher for longer” likely also applies for energy prices.

If an investor accepts the thesis that energy prices will remain higher for longer, Exxon Mobil is poised for an extended cycle of strong earnings. More concretely, with oil above $70/ barrel, I see Exxon sustaining a minimum 7% cash distribution yield in 2024; with likely further upside on an even higher energy prices.

Overall, I consider XOM stock undervalued at 8.3x P/CF and assign a Buy recommendation.

Oil Trade Is Back In Play

The key driving factor for oil prices is strong demand. In 2023, the global economy has been growing at a healthy pace, defying expectations for a recession. This has led to an unexpectedly high demand for oil. Meanwhile, the OPEC group has made the decision to reduce supplies, despite the stronger-than-expected economic activity, and rising oil prices. In fact, Riyadh and Moscow recently announced that they are extending their voluntary oil supply cuts of approximately 1.3 million barrel per day, which were originally slated to expire this summer. This, of course, raised concern that the supply deficit in oil markets will draw down inventory levels, with the International Energy Agency warning that OPEC cuts were “locking world oil markets into substantial deficit.”

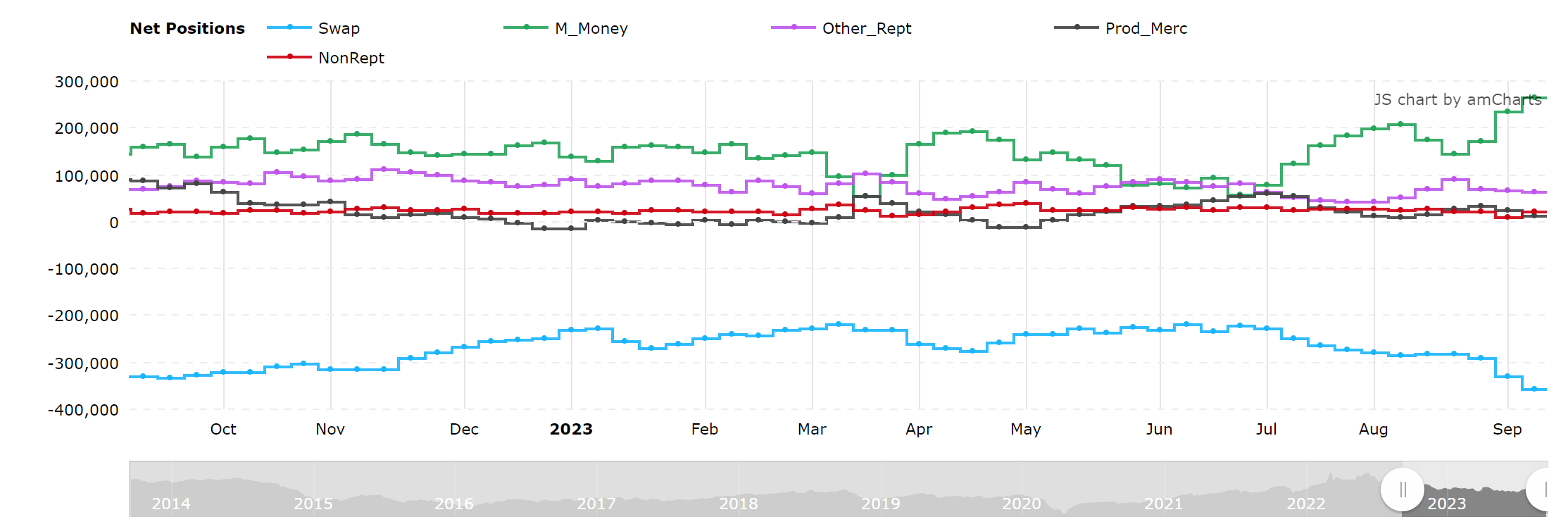

Unsurprisingly, hedge funds and other alternative asset managers have picked up on the demand vs. supply imbalance in the oil markets and added fuel to the price momentum, betting that prices will continue to rise. The latest COT report suggests that managed money long positioning in oil futures is at 12 months high, with the group being long 264 thousand contracts (equivalent to about five days’ worth of global demand).

Tradingster; COT

That said, it is worth considering that oil market look trapped in a self-reinforcing bullish cycle: Production cuts lead to tighter supply, pressuring prices upwards, which in turn attracts increased speculation by investors. Given this momentum, I would not find it surprising if the WTI futures for 2024 delivery close $100/ barrel by end of this year. This scenario is especially likely when considering that the global economy may accelerate in early 2024 on the backdrop of the first interest rate cuts.

Exxon: Making Big Money …

When oil was peaking in late 2022, Exxon was generating quarterly profits of $18-22 billion, with about $20-25 billion of operating cash flow. In Q2 2023, these figures dropped to $10.5 billion of profits and $9.3 billion of operating cash flow, respectively. So, I see two key benchmark takeaways here:

First, and this is the downside case, if the WTI benchmark remains in the $60-70/ barrel range, Exxon is likely to continue accumulating earnings of approximately $10 billion per quarter. Compared to a market capitalization of about $460 billion, the annualized earnings yield is implied at almost 10% — quite attractive, in my opinion.

The second takeaway relates to Exxon’s operating leverage and operating profitability at higher energy prices. Most notably, if we consider that oil pushes back to $100/ barrel, then investors may reasonably expect Exxon’s quarterly profits to edge again towards $20 billion, resulting in an annualized implied earnings yield of close to 20%.

… And Distributing Cash To Shareholders

Higher profits for a company do not necessarily equate to higher shareholder returns. For Exxon, however, the equation holds true. Reflecting on the past 24 months, it is evident that the major share of Exxon’s income is allocated to distributing cash to shareholders. And with a net negative financial position of only $12 billion ($41.5 of debt and $29.5 cash), this is unlikely to change going forward. In fact, as long as oil prices remain above $70/ barrel, I strongly believe that Exxon feels comfortable paying out $30 billion of cash annually, equating to an equity yield of between 7-8%. Notably, my estimate reflects a payout ratio as a percentage of operating cash flow of about 50%, giving Exxon room to invest $15-20 billion a year in CAPEX and paying down the remainder of the company’s net debt position.

For context, in the trailing twelve months Exxon…

Read More: Exxon: The Oil Trade Is Back On The Menu (NYSE:XOM)