Bjorn Bakstad

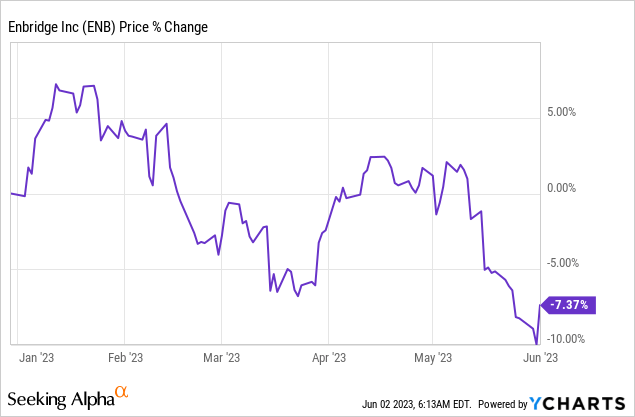

Enbridge (NYSE:ENB) is a well-run midstream firm whose shares have recently fallen to a new 2023 low. On the drop, I believe Enbridge is a very attractive dividend investment for investors. Enbridge is a Dividend Aristocrat and has paid a growing dividend for 28 years. The company’s first-quarter earnings card was also solid with high single digit adjusted EBITDA growth year over year and the midstream company confirmed its financial outlook for FY 2023 as well. Enbridge’s shares are very attractively valued on the drop and I have used the opportunity to buy the 2023 lows!

Pipeline and storage portfolio, predictable cash flows

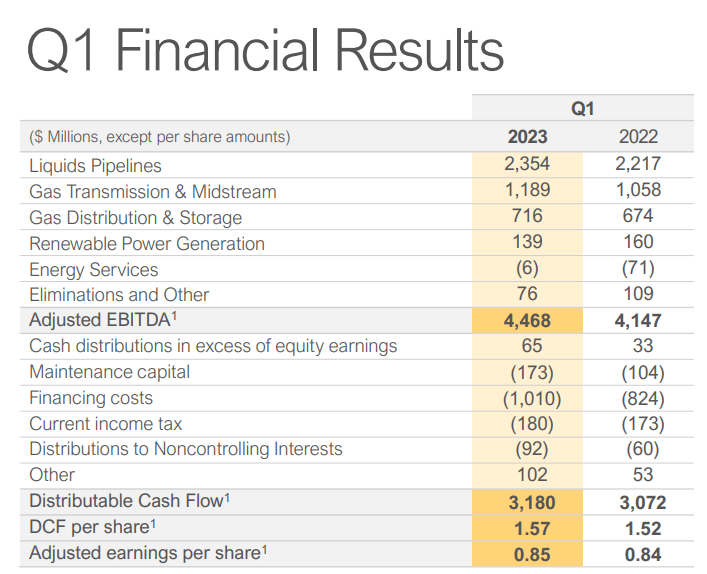

Enbridge is a diversified midstream company with liquids pipelines, natural gas delivery systems, storage facilities and a growing portfolio of on/offshore windfarm assets. Enbridge also delivered strong results for the first-quarter that I only want to touch on quickly. The company generated $4.5B in adjusted EBITDA, showing 8% year over year growth. Enbridge translates a big portion of this EBITDA into distributable cash flow which closed in on $3.2B in Q1’23.

Source: Enbridge

Enbridge generates the majority of its revenues from contracted delivery contracts that reduce the impact of price changes for energy products in the market. This results in an exceptionally high degree of cash flow predictability and a dividend that has a low risk of getting cut.

LNG export opportunity

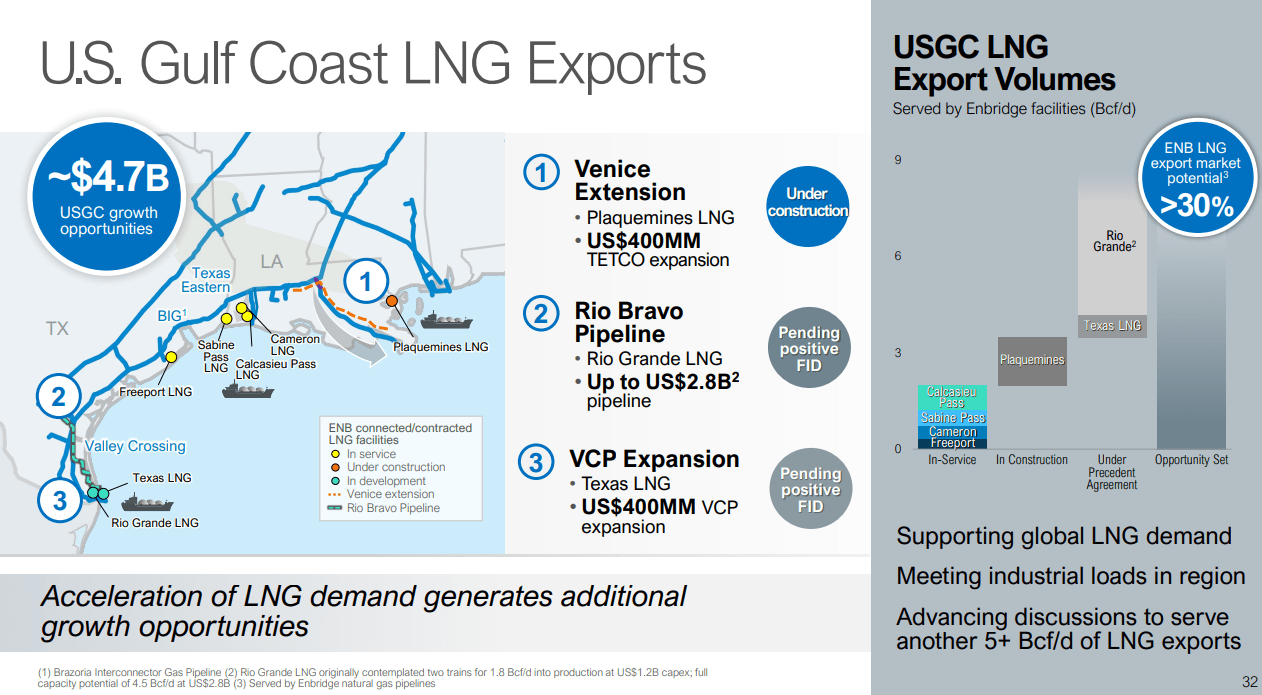

Enbridge is a leading midstream company with extensive pipeline networks in the United States and Canada and it has a huge growth opportunity in the U.S. Gulf Coast… which is an export center for liquified natural gas. The midstream company has said that it expects 30% growth in LNG export volumes, growth that is expected to come from expansion projects such as the Rio Bravo Pipeline. The Rio Bravo pipeline is expected to transport 4.5B cubic feet per day of natural gas from Agua Dulce in California to Brownsville in Texas.

Source: Enbridge

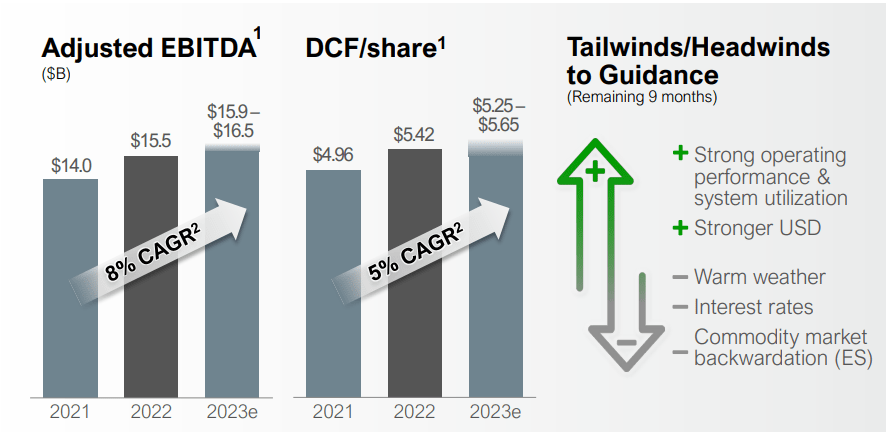

Financial outlook for FY 2023 confirmed, mid-to-high single digit growth in EBITDA, DCF

Enbridge has guided for $15.9-16.5B in adjusted EBITDA for FY 2023 earlier this year and the guidance range was confirmed when the company released first-quarter earnings. The midstream company also expects distributable cash flow in a range of $5.25-5.65 which is also unchanged from the company’s prior outlook. The distributable cash flow forecast implies approximately 5% year over year growth.

Source: Enbridge

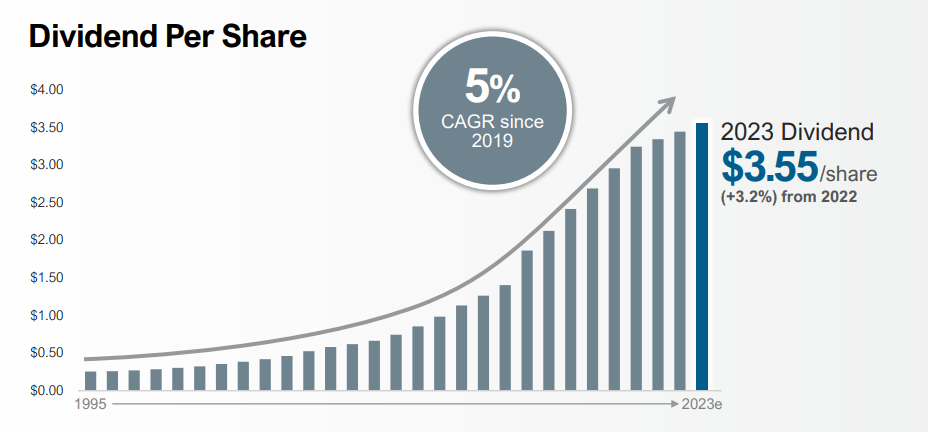

Enbridge’s yield, valuation vs. other midstream firms

Enbridge’s share price has fallen to a new 2023 low last week which I used to my advantage and added to my small holding. I believe the drop creates an attractive buying opportunity for dividend investors that want to buy a Dividend Aristocrat (those companies that raise their dividends for 25 years straight) at a decent price. Enbridge is a Dividend Aristocrat because the company has raised its dividend for 28 years and delivered 5% dividend growth since 2019. Enbridge pays out approximately 60-70% of its distributable cash flow so the company retains a lot of cash flow to invest in a diverse set of expansion projects.

Source: Enbridge

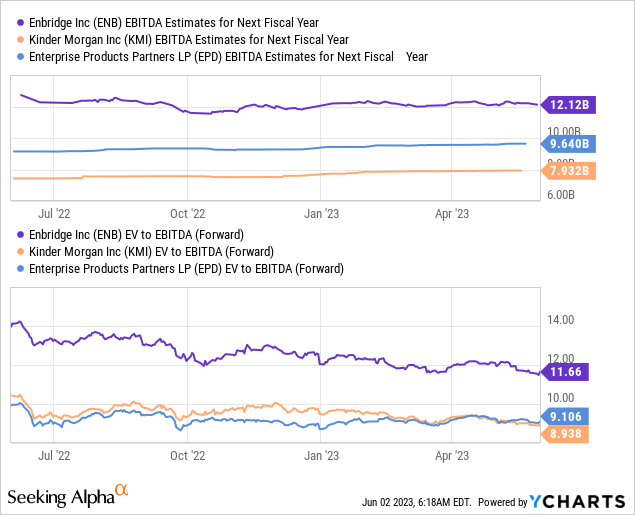

With a confirmed outlook in place and 5% DCF growth expected for FY 2023, Enbridge’s dividend yield of 7.3% looks solid to me. Based off of adjusted EBITDA, shares of the midstream firm are valued at 11.7X forward EBITDA which is slightly more expensive than the Enterprise-Value-to-EBITDA ratio of U.S.-based companies such as Kinder Morgan (KMI), Enterprise Products Partners (EPD) or Energy Transfer (ET). However, Enbridge deserves a Dividend Aristocrat premium and I am willing to pay such a premium if it means that the dividend will continue to grow going forward.

Risks with Enbridge

Enbridge is a fossil fuel-focused energy company which does a considerable amount of business in crude oil and gas… which exposes the company to regulatory headwinds in the context of a broader transition of the energy system. A shift towards alternative energy sources could benefit the company’s exposure to on/offshore windfarms but also hurt its core fossil fuel business. Regulatory limits on expansion projects, especially regarding Enbridge’s pipeline system, could result in lower EBITDA and distributable cash flow growth going forward.

Final thoughts

Enbridge is a well-run midstream firm that generates the majority of its revenues from contracted arrangements with its customers… which translates into predictable cash flow that support the company’s growing dividend. Enbridge confirmed its FY 2023 financial outlook and continues to expect high-single digit EBITDA and mid-single digit DCF per-share growth, and the company’s dividend is…

Read More: Enbridge Stock: High-Quality 7.3% Midstream Yield Available For Sale (NYSE:ENB)