Unlike the defaults during the Financial Crisis, this default cycle is structural, in addition to being financial.

By Wolf Richter for WOLF STREET.

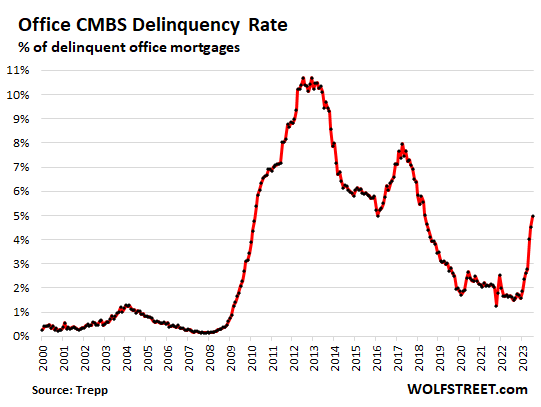

The delinquency rate of commercial real estate mortgages on office properties that had been securitized into Commercial Mortgage-Backed Securities (CMBS) spiked to 5.0% by loan balance in July, up from a delinquency rate of 2.8% in April, having now spiked by 2.2 percentage points in three months, by far the biggest three-month spike in the data going back to 2000, and by 3.4 percentage points so far this year, by far the biggest seven-month spike, according to Trepp, which tracks and analyzes CMBS.

This office-mortgage default cycle is outrunning the cycle during the Financial Crisis with ease, and it just started. The cycle during the Financial Crisis, as horrible as it was, started more slowly and proceeded more slowly than this cycle; it eventually topped out four years later with a delinquency rate of over 10% in 2012 and 2013. We’re already halfway there in seven months, on mortgages that were mostly written in 2014 and later.

Unlike the massive default cycle during the Financial Crisis, this default cycle is structural, in addition to being financial: No one knows what to do with all this vacant office space in older office towers. And cutting the rents to fill the properties – if it’s even possible to fill older office towers – won’t work because those much lower rents wouldn’t pay for the mortgage payments and expenses.

The default cycle is also financial in that CRE mortgage rates have more than doubled, which is a killer when on variable-rate mortgages and/or when a maturing mortgage needs to be refinanced. And at these mortgage payments, older office towers with a high vacancy rate doesn’t make economic sense anymore.

We have watched with fascination how mortgages on big office properties became delinquent, how landlords – giant landlords such as private equity firm Blackstone and private equity firm Brookfield – walked away from properties to let lenders take the losses, and this is happening from Houston to Chicago, from San Francisco to Manhattan, and all over the middle of the country.

And we have watched with amazement how the office market has un-frozen a little, finally, and some older office towers had actually sold, at huge discounts of 50% in Manhattan, of over 70% in San Francisco, of over 80% in Houston, and in one case, the largest office tower in St. Louis, it sold for so little in a foreclosure sale that all the proceeds were eaten up by fees and expenses, and lenders got zilch.

What all these big cases that came across our desk over the past 18 months had in common was that banks were not the lenders, that banks were not on the hook for losses on these big CRE loans, but that global investors ate those losses, because banks had securitized the mortgages and sold the CMBS to investors, or had sold the loans directly to private lenders, commercial mortgage REITs, and others.

This has espoused a perfectly logical theory around here that banks had kept the less risky office mortgages on their books, and sold their riskiest stuff to investors, and that smaller banks that piled into CRE lending mostly stayed away from refinancing big older office towers since 2014 – the kind that is now causing these mega-problems. The theory is that bank-held office loans would also face delinquencies and losses, but maybe not as badly as the stuff investors ended up with.

So some initial data on bank-held office loans going bad. The delinquency rate of bank-held office loans has also been rising since late last year: In Q4 2022, the delinquency rate of bank-held office loans reached 2.2%; and in Q1 2023 it rose to 2.7%.

This is according to Trepp’s analysis of Trepp’s Anonymized Loan-Level Repository data set, which is based on a sample of $160 billion in diverse bank loans from multiple banks. So this is a limited sample of the enormous size of the loan market, but it points at the direction this is going.

The data is quarterly. The delinquency rate of 2.7% in Q1, the last data point, is roughly equal to the March delinquency rate of office CMBS. So there’s that.

If this sample is broadly representative of all bank-held office mortgages, what we still don’t know is how big the loans are – they could be smaller office properties – and what the loss ratios will be if and when the properties are sold.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Read More: CRE Gets Messier: Office-CMBS Delinquency Rate Spikes the Fastest Ever.