Steve Jennings

Since going public, Coinbase (NASDAQ:COIN), the leading regulated exchange in the crypto space, has suffered a prolonged drawdown in its stock price. The day of the IPO was the company’s all-time high, and since then shares have sunk in basically a straight line.

While the fundamentals of the company leave something to be desired, the firm remains a bedrock crypto institution and household name. We believe that management is taking the right steps to diversify the company’s revenue base and cut bloat, which improves the fundamental side of the equation considerably. On the price action front, technical indicators suggest that the stock is oversold and poised for a rebound.

This setup presents an attractive opportunity for income-seeking investors. By employing a short put strategy, we can capitalize on this situation while minimizing risk and generating a solid chunk of income. With an extremely high probability of success, the trade idea we’ll outline is not only compelling, but also – we think! – the best risk adjusted way for everyday investors to potentially profit off of exposure to the crypto markets.

Financial Results

As we just mentioned, Coinbase has a rocky financial track record; it’s good to know that up front.

While the company remains capable of producing tremendous revenues and profits in bull/active crypto markets, cash flow dries up and the company dips into the red when interest in crypto dies down:

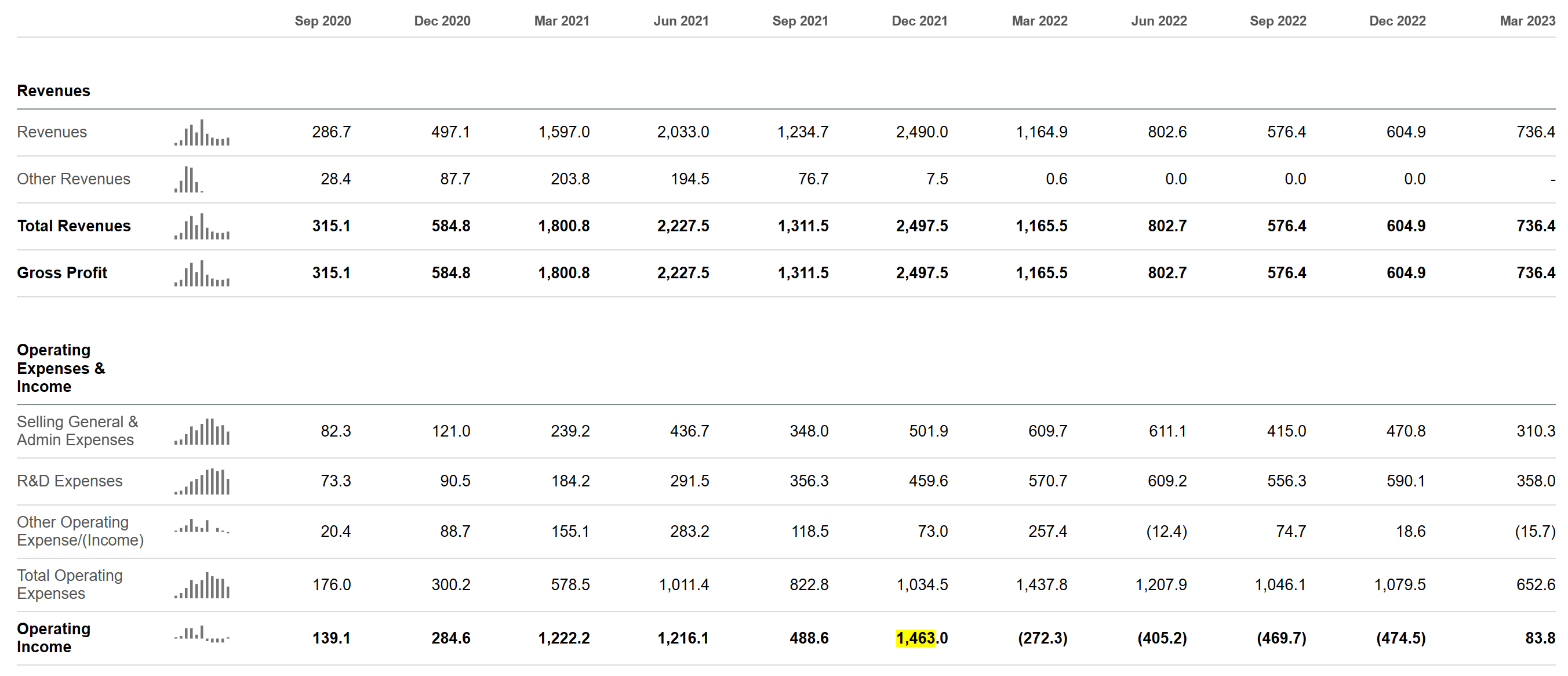

SeekingAlpha

At its peak in Q4 2021, COIN produced almost $1.4B in operating income, which is more than triple what Nasdaq (NDAQ) earned that same period. However, since that peak, operating results have been mostly lackluster.

Revenue declined 75% over the next 12 months from $2.4B to $604 million, and operating profits went into deep into the red.

The culprit here is Coinbase’s business model, which is mostly based around transaction revenue:

10K

COIN calls this “Net Revenue”. “Other Revenue” is stuff like Coinbase One (COIN’s subscription plan), Coinbase Cloud fees, Interest income, Custodial fees, and Blockchain Staking Rewards.

As you can see, as the crypto bear market took hold, transaction volume went down, and digital assets had their prices slashed in kind. This proved to be a 1-2 punch in terms of revenue impact, which caused the recent operating losses.

However, Brian Armstrong and management have shown keen awareness of this problem and continue to move towards diversifying the business away from pure maker/taker fees.

To this end, Coinbase is making serious moves. It has been reported that the firm is looking into starting an offshore futures exchange, and the company just announced the launch of Base, its own Ethereum L2 rollup chain. These initiatives and others should begin to shift the profile of Coinbase’s revenue in the future, which is beneficial for shareholders that have been on a bumpy ride so far.

Revenue is just half of the equation, though. Management also have a keen eye on expenses within the organization.

In the most recent quarter, Coinbase actually produced an operating profit for the first time since Q4 2021. With revenues still down more than 60% from highs, this recent profit is a consequence of management taking a serious axe to the company’s cost structure. And, given than revenue has begun to rebound over the last two quarters, it’s clear that this reduction in headcount and other spend is not having an impact on the success of the product.

As users ourselves, we can also say anecdotally that it seems that the company is moving faster to release better products, like the company’s recent TradingView integration into its PRO offering, and simplified / improved UI and UX.

Between the revenue mix strategy and cost structure agility, Coinbase has proven through the recent volatility that it has tremendous operating leverage, which is an excellent quality in a long-term investment.

Now that management has also “taken the hint” when it comes to profitability, it seems unlikely that costs will balloon again any time soon.

All in all, we think it’s a good time to get involved in the unfolding fundamental story.

Technicals

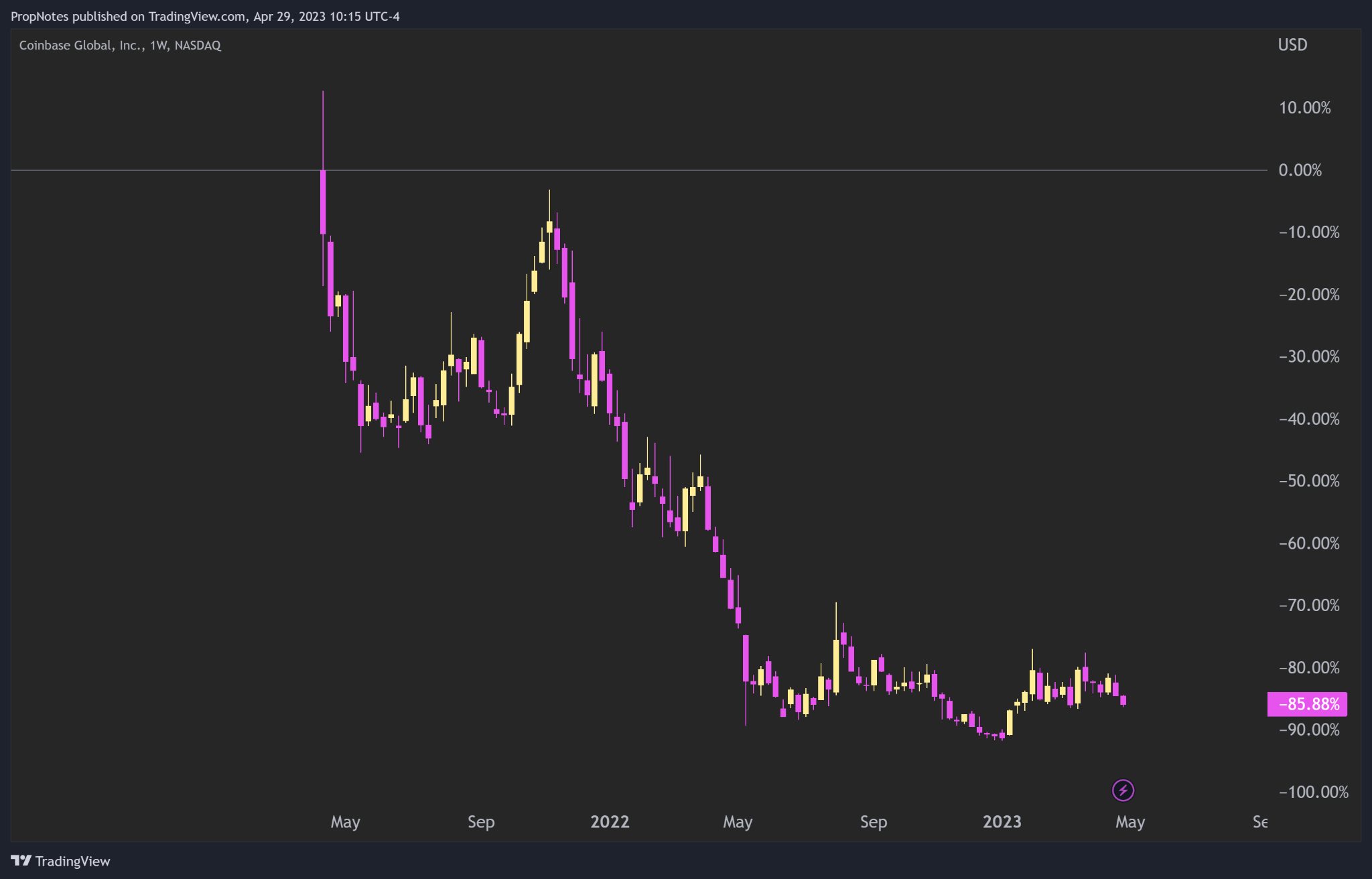

As we stated at the start, Coinbase shareholders have had a rough ride since IPO day:

TradingView

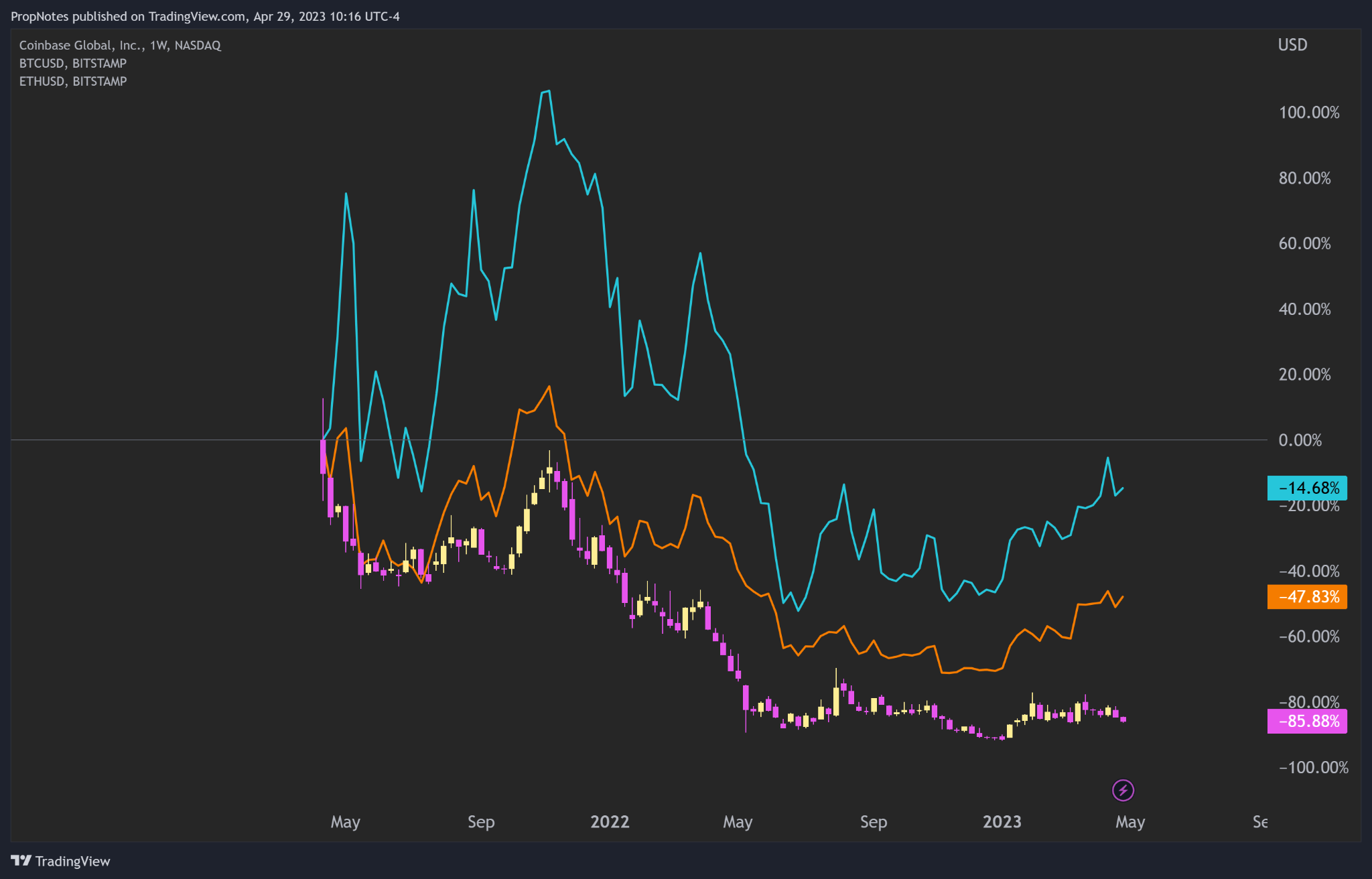

Shares have not only underperformed the market (which is obvious), but they have also underperformed the crypto market as a whole:

TradingView

Bitcoin and Ethereum have actually held up much better in the bear market for digital assets, which may surprise some investors.

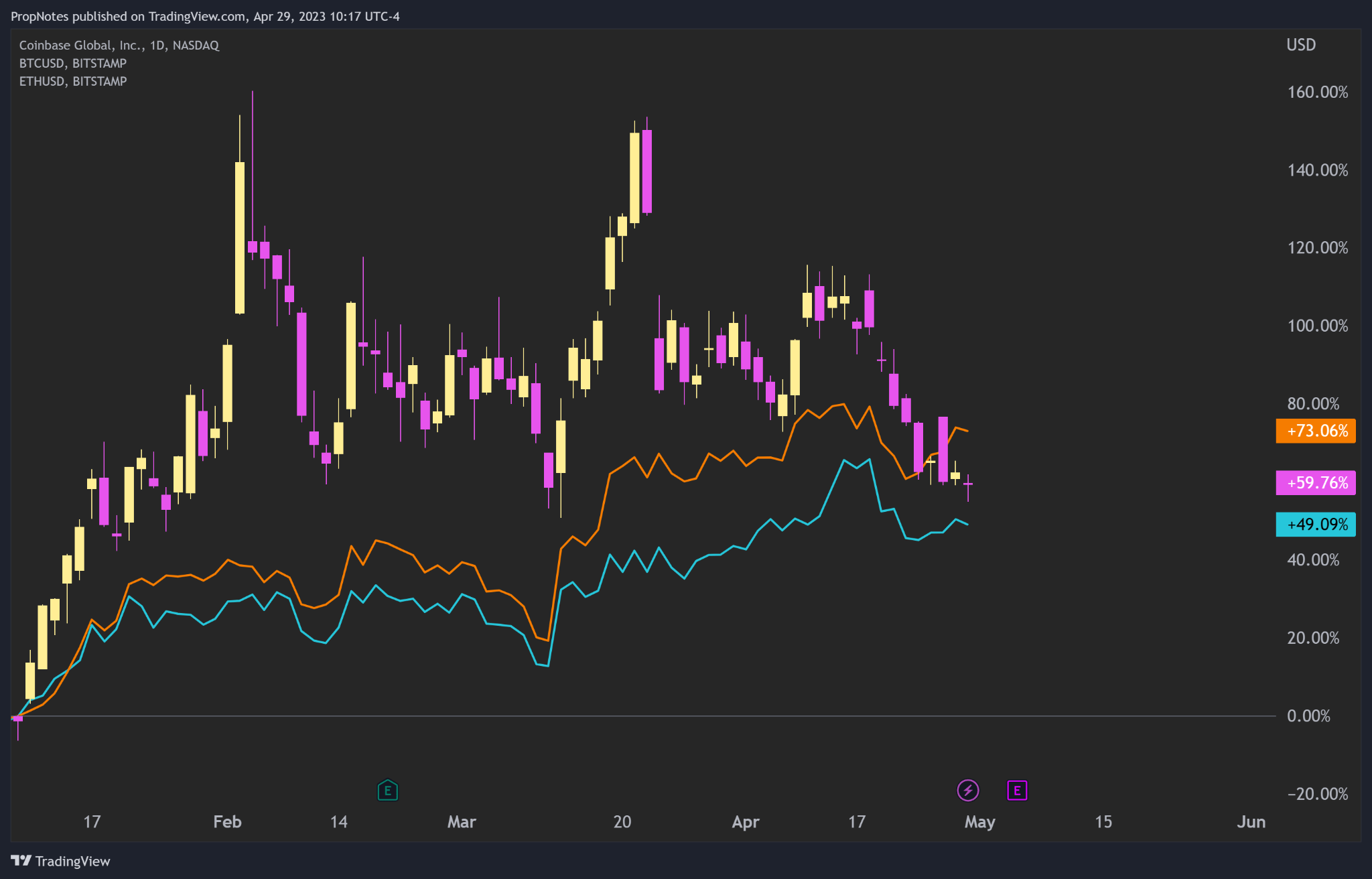

Conversely, COIN stock outperformed considerably in the first three months of this year when Bitcoin and Ethereum caught a bid:

TradingView

Taken together, COIN shares throughout history should be viewed as a leveraged proxy to mainstream crypto…

Read More: Coinbase: Diversifying Revenue And Well Positioned For Next Bull Market