zhengzaishuru

Baytex Energy (NYSE:BTE) closed on its acquisition of Ranger Oil in late June, resulting in increased production of approximately 155,000 BOEPD in 2H 2023. At current strip prices Baytex is now expected to generate US$426 million in free cash flow during the second half of 2023, benefiting from higher oil prices and reduced heavy oil differentials.

I now estimate Baytex’s value at around CAD$7.45 (US$5.50) per share at long-term $75 WTI oil. This also assumes a US$15 WCS differential. Stronger near-term oil prices plus the improved heavy oil differentials have resulted in a 13% increase in my estimate of Baytex’s value compared to March 2023.

This report uses US dollars unless otherwise indicated, as well as an exchange rate of US$1.00 to CAD$1.35.

Baytex’s Assets And Capital Allocation

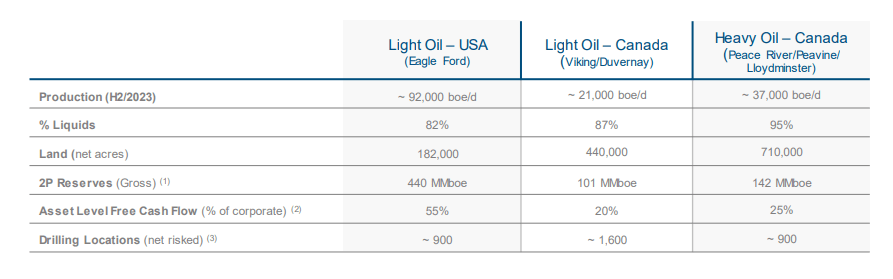

Baytex now has approximately 59% of its production and 55% of its asset level free cash flow coming from the Eagle Ford. The remaining 41% of Baytex’s production and 45% of its asset level free cash flow comes from its Canadian operations. Baytex’s Heavy Oil assets account for the majority of its Canadian production, although the margins are typically lower than its Light Oil assets due to the heavy oil differentials.

Baytex’s Business Units (baytexenergy.com)

Baytex is currently putting approximately 70% of its 2H 2023 capex budget towards the Eagle Ford, with the remainder split between its Canadian Light Oil and Heavy Oil assets.

Baytex’s Capex (baytexenergy.com)

Outlook For 2H 2023

Baytex expects production to average approximately 155,000 BOEPD in the second half of 2023. This includes full contribution from the Ranger Oil acquisition that closed late in Q2 2023.

Baytex’s production mix during this period is expected to be 50% light oil, 22% heavy oil, 12% NGLs and 16% natural gas.

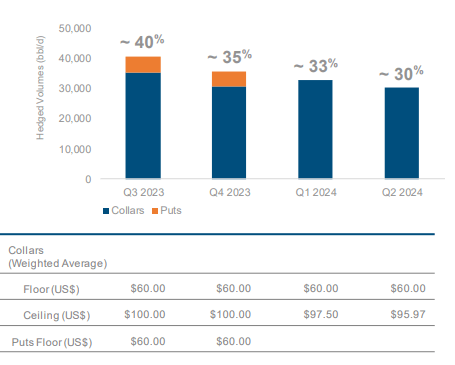

At current strip (including roughly $83 WTI oil) for the second half of 2023, Baytex is expected to generate $1.684 billion in revenues, inclusive of hedges. Baytex’s oil collars are quite wide, so they won’t affect Baytex’s results unless oil prices move significantly from current levels.

Baytex’s Hedges (baytexenergy.com)

Baytex is benefiting from relatively strong oil prices (with 72% of its production being oil) as well as relatively narrow heavy oil differentials. Baytex’s heavy oil production may realize around $59 per barrel for 2H 2023, while its light oil production should realize over $80 per barrel.

|

Units |

$ Per Unit |

$ Million USD |

|

|

Heavy Oil |

6,274,400 |

$59.00 |

$370 |

|

Light Oil |

14,260,000 |

$82.00 |

$1,169 |

|

NGLs |

3,422,400 |

$22.00 |

$75 |

|

Natural Gas |

27,379,200 |

$2.60 |

$71 |

|

Hedge Value |

-$1 |

||

|

Total |

$1,684 |

Baytex’s royalty rate during the second half of the year may end up around 22.5% due to higher commodity prices and the higher royalty rates with the Ranger assets (compared to Baytex’s Canadian assets). One of Ranger’s presentations indicated a roughly 23% royalty rate.

Post-acquisition, Baytex’s operating expenses may average around US$8.50 per BOE, while its 2H 2023 capital expenditures are expected to be around US$460 million.

|

$ Million USD |

|

|

Royalties |

$379 |

|

Operating Expenses |

$242 |

|

Transportation |

$44 |

|

General And Admin |

$40 |

|

Cash Interest |

$75 |

|

Capital Expenditures |

$460 |

|

Leasing Expenditures |

$7 |

|

Asset Retirement Obligations |

$11 |

|

Total Expenses |

$1,258 |

This leads to a projection of US$426 million in free cash flow for Baytex in 2H 2023. Baytex had mentioned expectations for around US$300 million in 2H 2023 free cash flow before, but that was at $75 WTI oil for the second half of the year.

Debt And Dividends

Baytex had 862.2 million common shares outstanding at the end of Q2 2023, and then repurchased 4.7 million common shares between July 1st to July 26th at an average price of CAD$4.59 (US$3.40) per share. This would have cost Baytex approximately US$16 million.

Baytex is paying a quarterly dividend of CAD$0.0225 (US$0.0167) per share on October 2 to shareholders of record on September 15, 2023. This is Baytex’s first dividend since 2015 and currently adds up to around US$14 million per quarter.

Baytex reported having approximately US$2.11 billion in net debt at the end of Q2 2023. It may be able to reduce its net debt to US$1.9 billion by the end of 2023 if it puts 50% of its free cash flow towards its base dividend plus share repurchases.

Estimated Value

I am maintaining my view on long-term WTI oil prices at $75, but Baytex is benefiting from both improved near-term oil prices and narrower heavy oil differentials.

If WCS differentials can average US$15.00, then I’d now value Baytex at approximately CAD$7.45 (US$5.50) per share in a long-term $75 WTI oil scenario. This also assumes that commodity prices follow the current strip (including $80 WTI oil) for 2024,…

Read More: Baytex Energy: Strong Oil Prices Push Projected 2H 2023 FCF Above $400 Million