Pgiam/iStock via Getty Images

My thesis

ABM Industries (NYSE:ABM) is a dividend king. Its business demonstrates steady revenue growth with more-or-less stable profitability ratios. The stock might be a robust short-term safe harbor during panic in growth stocks, but it is quite unlikely that its revenue growth will suddenly spike considering the maturity of industry the company represents. Profitability ratios are inherently low, and it is the reason why notable investments to spur growth are quite unlikely to happen. The dividend yield is lower than current inflation levels and the stock’s valuation does not look attractive. With no apparent strengths apart from the dividend king status, I am neutral about ABM and assign it a Hold rating.

ABM stock analysis

The company is a provider of integrated facility solutions worldwide. In FY 2023 the company generated 93% of its revenue domestically. These solutions include janitorial, energy, facilities engineering, electrical and lighting, landscape and turf, HVAC and mechanical, mission critical, and parking solutions.

ABM’s FY 2023 10-K

ABM’s reportable segments are Business & Industry ((B&I)), Manufacturing & Distribution (M&D), Education, Aviation, and Technical Solutions. B&I (providing services to commercial real estate properties, sports and entertainment venues, and traditional hospitals and non-acute healthcare facilities) is the company’s largest segment and it generated half of ABM’s revenue in 2023.

ABM’s FY 2023 10-K

From the perspective of service lines, Janitorial is the largest representing 62% of the total revenue in FY 2023. According to the 10-K, Janitorial arrangements provide a wide range of essential cleaning services for a wide array of facilities types. These arrangements are often structured as monthly fixed-price, square-foot, cost-plus, and work order contracts. Understanding the major service line is crucial because it significantly affects the company’s performance and future prospects.

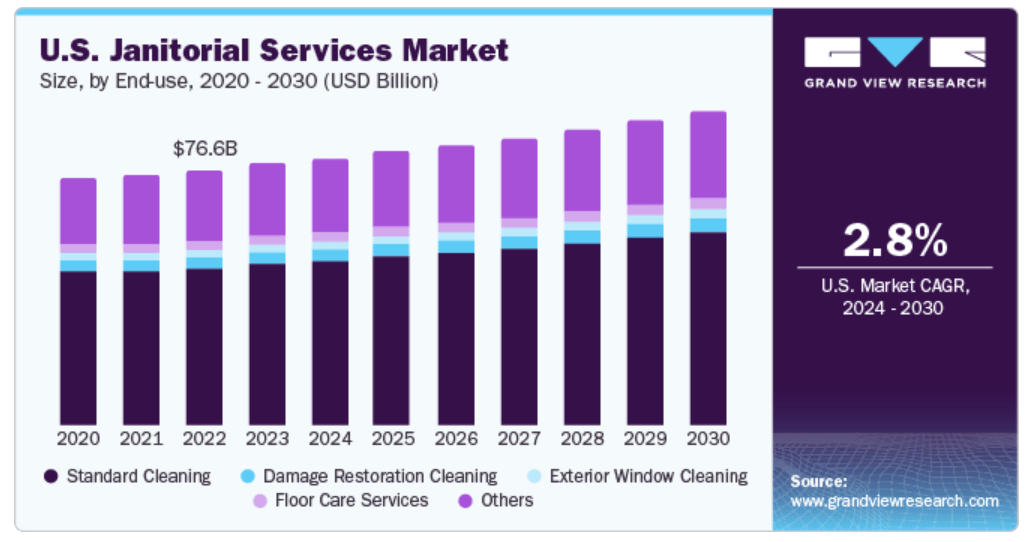

Grand View Research estimates the U.S. janitorial services market size at $78.2 billion. This means that ABM holds a notable 6.4% share in the U.S. janitorial market. On the other hand, the market is extremely mature and is expected to grow with a 2.8% CAGR, close to historical inflation levels. This means almost no growth in real terms, not a good sign for investors.

Grand View Research

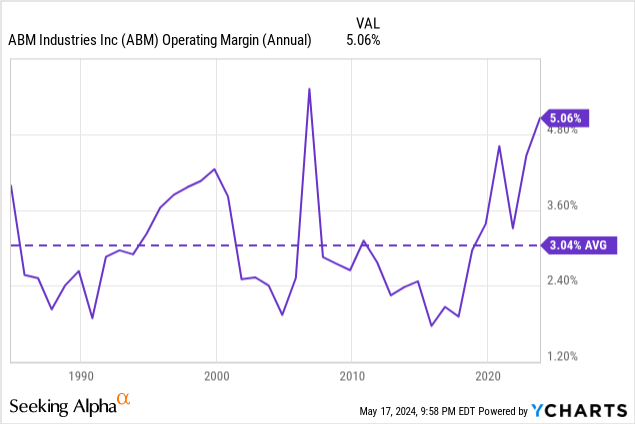

The janitorial industry is labor intensive as common services require physical exertion and manual labor. Therefore, this business faces substantial wages growth pressure on the bottom line and is poised to experience it further. Wages growth is moderating but it is still close to 5%, beyond the projected janitorial industry growth. Due to low barriers to entering the market, it is highly competitive, which does not allow players to exercise pricing power. Therefore, operating margins are low and we can see it from ABM’s income statement.

According to the above chart, ABM’s long-term operating margin’s average is 3% and it rarely achieved even 5%. Having a 3-5% operating margin means that profitability can move close to zero in case of adverse conditions like the demand for services dropping due to the weak macroeconomic environment or rapidly increasing inflation. With thin operating margins it is impossible for a company to have a strong balance sheet. ABM’s net debt position has almost doubled over the last five years, which is also a warning sign for investors, especially considering that the business is asset lite and does not require large capex amounts.

Seeking Alpha

In light of the net debt ramping up rapidly, the company’s dividend policy and aggressive buybacks are questionable. If this trend continues, the company’s “dividend king” status might be at risk.

Overall, I do not expect robust positive catalysts to unlock in the foreseeable future for ABM. Revenue dynamic is expected to move approximately in line with inflation and wages growth will likely continue pressuring the company’s profitability. In this reality, it is difficult to expect any sudden growth, especially considering the company’s weakening financial position.

Intrinsic value calculation

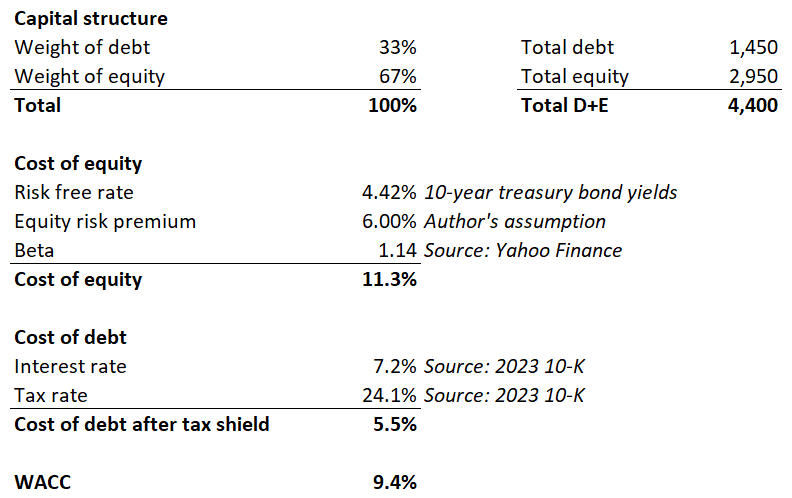

Calculating discount rate is crucial for a valuation analysis because valuation analysis is mostly about future cash flows or dividends growth. In the below working I show my WACC calculation using the CAPM model. All assumptions are outlined, and sources explained. According to the working, ABM’s WACC is 9.4%.

DT Invest

The only ABM’s strength that I see is its reputation as a “dividend king”. Therefore, to value the stock I will use a dividend discount model (DDM) approach. Cost of equity is used as a discount rate for DDM, which is 11.3%, according to the above working….

Read More: ABM Industries Stock: Dividend King Without Robust Positive Catalysts (NYSE:ABM)