La_Corivo

Introduction

Pan American Silver (NYSE:PAAS) is one of my favorite silver miners. Since Yamana’s acquisition, the company has added quality assets, considerably expanding its reserves and resource base. PAAS assets are in countries with relatively low political risk in the Western Hemisphere. Besides that, the revenue per country does not exceed 25%.

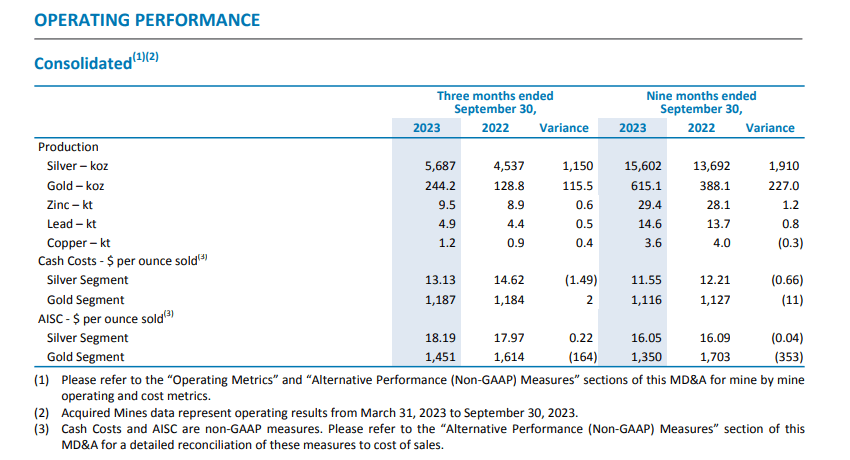

3Q23 production figures were not impressive at first glance, being on the lower limit of the guidelines. Despite that, PAAS output grew significantly due to the acquisition of Yamana assets. Silver cash costs declined, resulting in lower AIC. 3Q23 net income is still negative, although the operating cash flow increased 100% YoY.

The company has sound financials with $356 million cash and $830 million total debt (including leases). PAAS profit margins have improved over the last few quarters. PAAS trades at 2.9 EV/Sales, 11.5 EV/EBITDA, and 1.1 P/BV. Price action is supportive for initial longs. Adding the macro tailwinds being long silver and gold miners is a wise decision. I give PAAS a buy rating.

3Q23 results overview

In 3Q23, PAAS produced 5.7 M oz of silver and 244 k of gold. Gold production falls below 3Q23 guidelines, while silver production is on the lower limit. The silver production 3Q23 increased by 25% YoY, driven by Yamana assets, which added 2.37 M oz of silver. Gold production in 3Q23 doubled compared to 3Q22. Yamana mines added another 128 M oz of gold to PAAS’s quarterly gold output.

The table below shows 3Q23 production figures.

PAAS 3Q23 report

Silver segment

Due to ventilation issues, La Colorada mine in Mexico delivered 1 M oz silver in 3Q23, or 32% lower than in 3Q22. PAAS has advanced the construction of concrete-lined ventilation shafts. The plan is to reach a depth of 593 meters in 4Q23. In 3Q23, the excavation achieved 522 meters. By mid-2024, exhaust fans are planned to be installed.

Cerro Moro is from the newly acquired assets. PAAS has invested $14 million since the acquisition in March 2023. In 3Q23, the mine delivered 2.66 M oz of silver and 54.4 k oz of gold. Silver cash costs were negative, at $0.08/oz, and AISC was $5.8/oz.

Huaron mine in Peru produced 0.9 M oz silver in 3Q23, or 5% compared to 3Q22. The main driver is the improved ore grades. Base metals production grew significantly YoY, copper by 37%, zinc by 6%, and lead by 20%. Higher ore grades and improved recovery for copper contribute to increased output in 3Q23. Cash costs grew by $1.0/oz, caused by rising refining charges and lower by-product credits. The latter declined due to lower zinc prices. AISC grew by $4.3/oz due to increased sustaining capital expenditures.

San Vincente mine had a strong 3Q223, scoring higher production figures across all metals. Silver output grew by 11% YoY, zinc by 7%, lead by 19% and copper by 53%. Higher ore grades and increased throughput contributed to the rising quarterly production. 3Q23 cash costs were $6.21/higher than 3Q22 due to the timing of zinc and silver concentrate shipments, resulting in lower by-product credits. AISC increased by $7.88/oz YoY.

3Q23 silver cash cost is lower than 3Q22 cash costs ($14.6/oz). The decline is due to higher gold by-product credits from Cerro Moro and lower OPEX costs at the Manantial mine, which is in care and maintenance. La Colorada mine had lower ore grades and by-product credits from declining base metals production (lead and zinc). Silver cash costs YTD remain lower than 2022 YTD for the abovementioned reasons. Silver AISC in 3Q23 grew by $0.22 compared to 3Q22. Huaron and San Vincente required higher sustained capital investments, increasing AISC. Silver AIC in 3Q23 was $18.19/oz and cash cost was $13.13/oz. Both slightly exceed the 2Q23 guidelines figures.

Gold segment

PAAS Jacobia and El Penon were acquired from Yamana. The former produced 96.6 k oz of gold for 2Q23 and 3Q23 at $808/oz cash cost and $$1,146/oz AISC. PAAS has invested $30.2 million since the acquisition. El Penon mine produced 2Q23 and 3Q23 2.05 M oz gold at $1,020/oz cash cost and $1,213/oz IASC. The lower-than-expected ore grades caused declining production. PAAS invested $11.6 million in mine equipment upgrades and exploration.

Gold cash costs were $1,187/oz in 3Q23, while 3Q22 cash cost was $1,184/oz. The challenging ground conditions in Timmins mine in Canada resulted in lower production figures. Minera Florida also added pressure on the cash costs as a higher-producing mine. On the positive side, Jacobina balanced the adverse developments as a lower-cost producing mine. Gold AISC fell by $164 YoY to $1,451/oz in 3Q23.

Other highlights from 3Q23

On November 6, 2023, PAAS completed the divestment of the Agua de Falda (ADFL) project. The company had a 57% interest in ADFL; Nacional del Cobre de Chile…

Read More: Pan American Silver: Diversified Precious Metal Miner With Robust Balance Sheet