harmatoslabu

Natural gas has faced an incredibly tumultuous period over the past two years. Natural gas prices initially skyrocketed in 2021 due to shortages created during COVID-19 lockdown production cuts. The commodity continued to rise in 2022 as the Russia-Ukraine war led to greater EU demand for US exports and immense speculation surrounding future demand needs. I became bearish on natural gas in mid-2022 due to unreasonable expectations surrounding EU demand needs. However, I have had a bullish view of the commodity since spring, as lower prices have indicated production cuts amongst most US producers. Since then, natural gas has increased slightly, leading to added performance for critical producers such as EQT Corporation (NYSE:EQT).

Bullish investors in natural gas have multiple options. The natural gas futures ETF (UNG) is one option, but it often chronically underperforms due to harmful contango decay in the futures curve. EQT Corporation is an interesting alternative because its production is highly concentrated in natural gas. While it does not face contango risk, it faces risk relating to increasing production costs and potential overvaluation.

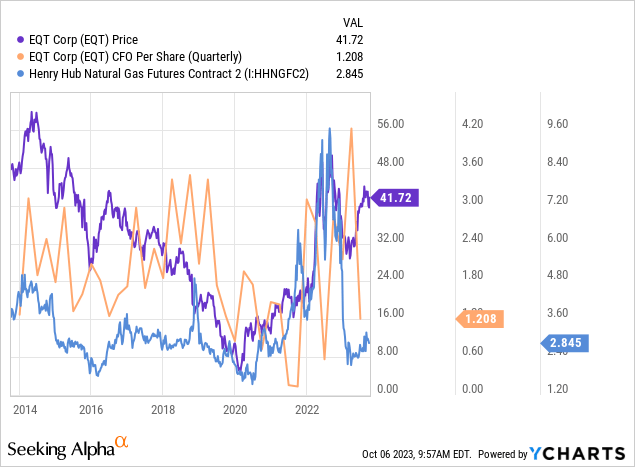

Historically, both EQT’s price and cash flow per share correlate to the futures price of natural gas. Usually, some portion of EQT’s production is hedged, so its correlation to natural gas is not perfect. Last year, it had solid cash flows due to the high price of natural gas. However, gas has crashed to extreme lows since then, pushing its operating cash flow to near-zero levels. Despite this, EQT’s share price remains nearly the same level during the 2022 peak. See below:

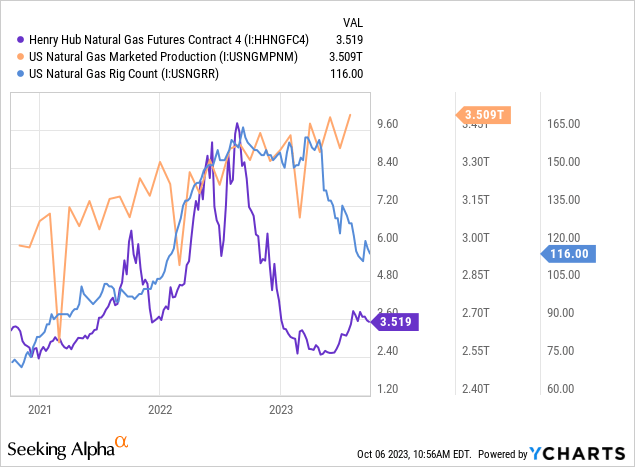

EQT did not entirely benefit from 2022 natural gas prices due to its hedge ceilings last year, making its profit outlook today nearly equal to its profits in 2022. Many factors may impact the company, mainly changes in production costs and natural gas prices. Natural gas is relatively cheap today but is more stable as its production outlook stagnates. Overall, I expect natural gas prices to stabilize around the $3-$3.5 level in 2024, given the trend in the natural gas rig count; however, upcoming winter weather conditions will play a key role in its 2024 pricing.

EQT is Cheap, Given the Rising Henry Hub Price

Most of EQT’s 2023 production is covered by basis hedges of around $4.25/MMBTU level, while, at the end of Q2, 30% of its 2024 production was hedged at $3.64/MMBTU. The breakeven cost of its output varies from around $2/MMBTU to $3/MMBTU across its portfolio. Thus, looking into its 2024 potential, we will need to closely monitor that range to determine its ability to generate a profit. We know that nearly a third of its portfolio is hedged and at a slightly profitable level. Still, given that natural gas has held the $2-$3 range this year, the company will unlikely continue to hedge its 2024 production.

The 2024 Henry Hub futures contracts are trading at ~$3.4/MMBTU, up by around $1/MMBTU over recent months, putting pricing back into a firmly profitable range for the company. The rise in natural gas prices may likely result from the sharp decline in the rig count, associated with profit declines amongst most US natural gas producers. That said, total US natural gas production remains very strong today. See below:

As stated in its last presentation, this “breakeven” level includes capital costs, corporate overhead, taxes, and other key expenses. Over the first half of 2023, EQT had 883K MMcf in sales volume, or ~1.83B MMBTU annualized. That said, the company expects 1.9-2K Mcfe in total 2023 production, so I will project its 2024 production at 2.02B MMBTU, of which about 639M was hedged at the end of Q2 at a weighted-average floor of $3.64. Assuming an all-in breakeven of around $2.5/MMBTU, we can expect around $728M in profits from its hedged position. Further, if natural gas remains around $3.4 (based on 2024 average contracts, marginal profit of ~$0.9/MMBTU), its total profit on unhedged positions should be around $1.24B. Together, its full natural gas expected profit is ~$1.97B. Accounting for oil, NGL, ethane, and other products, which usually account for 10% or less of its revenue, I expect combined segment profits of ~$2.1B.

The variability in profit potential is significant at potentially +/- $1B, given no change in commodity prices but variation in production costs across its operating segments. Its Pro Forma free-cash-flow breakeven cost is around $2.15/MMBTU, meaning it should earn around $952M in FCF on its hedged position and ~$1.65B on its non-hedged position, assuming no change in commodity prices and production costs. Together, adding potential FCF from other segments, I forecast its 2024 FCF at ~$2.7B based on these assumptions.

EQT Corporation Stock: Strong Value Potential In Healthy Natural Gas Market