PM Images

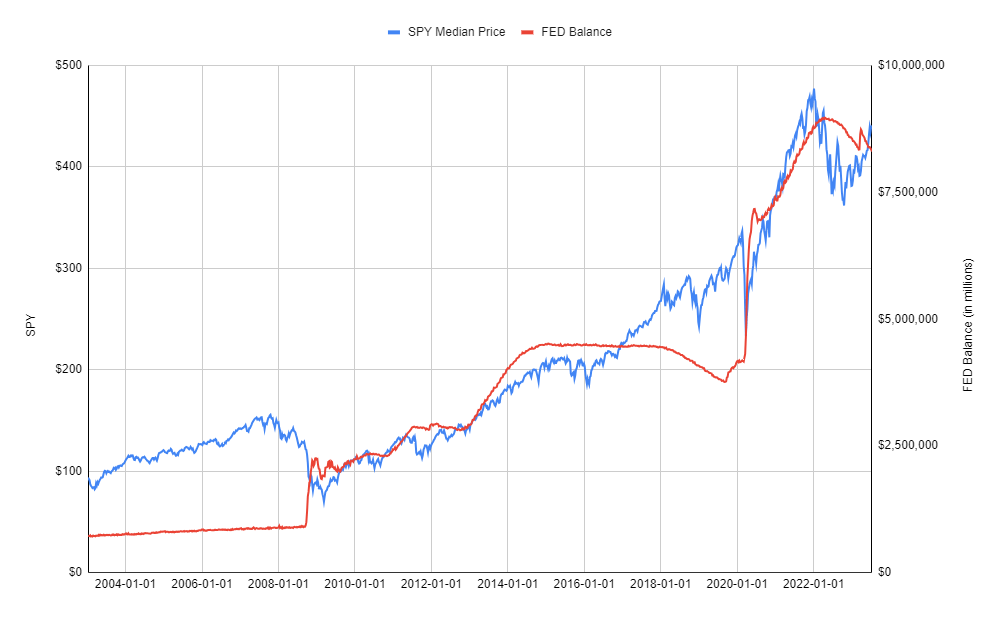

When the COVID-19 pandemic hit the United States in early March 2020, the Federal Reserve (FED) swiftly responded to limit the economic fallout. It adopted a range of measures, including reducing its interest rate target to near zero and implementing large-scale purchases of U.S. Treasury bonds and mortgage-backed securities (MBS). These actions, known as quantitative easing (QE), involved injecting reserves into the banking system. As a result of these purchases, the Fed’s balance sheet grew from around $4 trillion prior to the pandemic to nearly $9 trillion by the beginning of 2022.

Quantitative Easing vs Tightening

QE had first been employed by the Fed more than a decade ago as an unconventional monetary policy tool during the Great Recession. However, its return during the COVID-19 crisis suggests that it has become a more routine part of the Fed’s crisis toolkit. Nevertheless, economists continue to debate the effectiveness of QE and have limited knowledge about the reverse process of shrinking the Fed’s balance sheet, known as quantitative tightening (QT).

In response to inflation running well above its long-term target, the Fed began unwinding its accommodative monetary policy in 2022. This involved ending QE in March and commencing QT in June. When QE concluded, the Fed reinvested any maturing securities to maintain the size of its balance sheet. With QT, the Fed ceased reinvesting up to $30 billion in maturing Treasuries and $17.5 billion in maturing MBS each month, thereby passively shrinking its assets as those securities matured without being replaced. The caps on reinvestments then increased to $60 billion and $35 billion, respectively, in September 2022.

FRED Data vs SPY Price (Google sheets chart)

The primary goal of QE is to reduce long-term interest rates. By buying long-term assets, the Fed reduces their supply, thereby increasing their price and lowering their yield. Lower interest rates can stimulate economic activity by reducing the cost of borrowing. While some economic models suggest that QE should have little effect since it swaps one type of government liability for another, there are other theories that explain how it stimulates the economy. For instance, certain financial firms may have preferences for holding long-dated securities, and QE can also provide a signal about future Fed policy and improve liquidity conditions in financial markets.

In contrast to the debates surrounding QE, there is considerably less certainty regarding the effects of QT. The Fed’s experience with shrinking its balance sheet is limited to the previous episode from 2017 to 2019, and even then, the available empirical evidence is scarce. A recent study by economists at the Fed Board of Governors estimated that reducing the balance sheet by approximately $2.5 trillion over several years would be roughly equivalent to raising the Fed’s policy rate by half a percentage point. However, the authors emphasized the considerable uncertainty associated with this estimate.

One key difference between QE and QT lies in their signaling effects. QE typically involves a swift and somewhat surprising response by the Fed during financial crises, which helps reassure markets. In contrast, the Fed has been cautious with QT, providing ample advance notice and following a fixed schedule to avoid market surprises. The Fed’s approach to QT reflects its desire to focus market attention on the federal funds rate as the primary monetary policy instrument. While QT may not produce significant announcement effects like QE, it has been found to have stronger liquidity effects.

Shrinking the balance sheet through QT serves several purposes. It provides additional monetary tightening to bring inflation back to the Fed’s 2 percent target. Furthermore, it helps mitigate the interest rate risk faced by the Fed as it raises rates. When the Fed tightens monetary policy and increases the interest it pays on reserves, it risks paying out more on its liabilities than it earns on its assets since rates on liabilities will rise while rates on assets remain largely fixed. Shrinking the balance sheet reduces the likelihood of the Fed recording losses and enhances the credibility of its monetary policy.

Moreover, the composition of the Fed’s assets is another reason for implementing QT. The Fed holds a significant amount of MBS, but its plan for reducing the balance sheet expresses a long-term preference for holding primarily Treasuries. Policymakers and economists argue that decisions regarding the allocation of credit to different sectors of the economy should be made by Congress or the Treasury Department, rather than the Fed. However, reaching a Treasuries-only balance sheet may take time, as the pace of MBS maturing and rolling…

Read More: The Risks Of Draining Liquidity: How Quantitative Tightening Impacts The Stock